How To Make Use of the Current Generous Estate Tax Environment if You’re Caught in the Middle

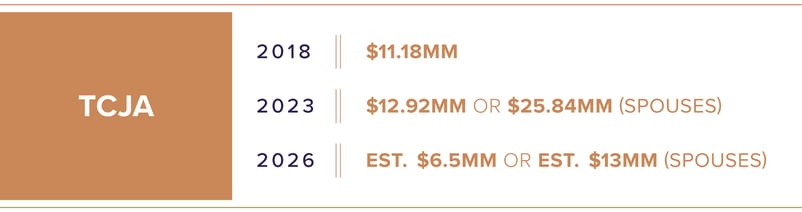

Since the Tax Cuts and Jobs Act (“TCJA”) was passed in 2017, the very high net worth (“VHNW”) segment of wealthy families in the US (generally those with investable assets of $5MM to $30MM) have been lulled into a sense of complacency. The TCJA doubled the estate exclusion amount from around $5.49MM per individual in 2017 to $11.18MM in 2018. Since, the exclusion amount has increased steadily with inflation to $12.92MM in 2023. As such, wealthy married couples can leave $25.84MM in 2023 to their heirs without having to worry about incurring an estate tax (state estate taxes are a different discussion).

However, changes are coming. Absent any legislation extending or modifying the current estate tax laws which seems highly unlikely in today’s political climate and the dismal state of the Federal deficit, the exemption amount is scheduled to revert back to pre-TCJA amounts (inflation adjusted) to around $6.5MM per individual, or $13MM for married couples beginning in 2026.

According to Wealth-X, a global leader in curating information on the wealth accumulation and activities, there were more than 950,000 VHNW individuals in the US in 2021, and they forecast the population of VHNW individuals to rise to 1.5MM people in North America by the end of 2025. The VHNW wealth segment sits squarely in the range of taxpayers who may be most impacted by a reversion to pre-TCJA estate tax laws.

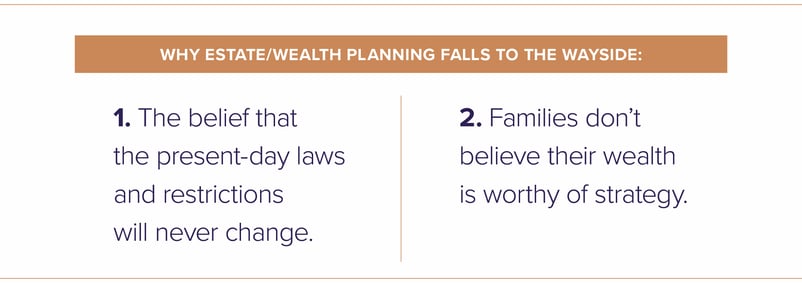

For many VHNW families, estate and wealth transfer planning has not been a priority for two primary reasons. The first reason is an unfounded belief that the historically generous estate, gift and GST tax laws in place today will simply not be allowed to sunset, and thus will remain in effect indefinitely. The second, and likely more prominent reason, is that these families simply do not feel wealthy enough to relinquish long-term enjoyment and utilization of a significant portion of their assets, as is required in many of the traditional wealth transfer planning strategies, such as family limited partnerships, grantor retained annuity trusts, IDGTs and other traditional planning techniques. After understanding that use of the Federal exemption amount builds from the ground up (meaning you must transfer more than $6.5MM or $13MM out of your estate in order to start making use of the pre-sunset exemption levels), VHNW families are even more discouraged from implementing significant tax saving planning strategies.

While implementing meaningful estate planning strategies to make use of the high exemption levels for the VHNW segment may seem unattainable given the uncertainty of the landscape and the constraints of the estate, gift and GST tax system, planning solutions have been refined over recent years that make effective strategies more palatable. However, those utilizing such strategies must still be well aware of the trade-offs and risks, and the potential for more accommodative political environments in both directions depending on the elections next year.

Effective solutions for the VHNW tend to center around two primary objectives: (1) preservation of some degree of access to and enjoyment of assets, and (2) the use of illiquid assets to minimize the impact on their current lifestyle and spending patterns. As such, there has been a revitalization and newly found emphasis on the following planning techniques.

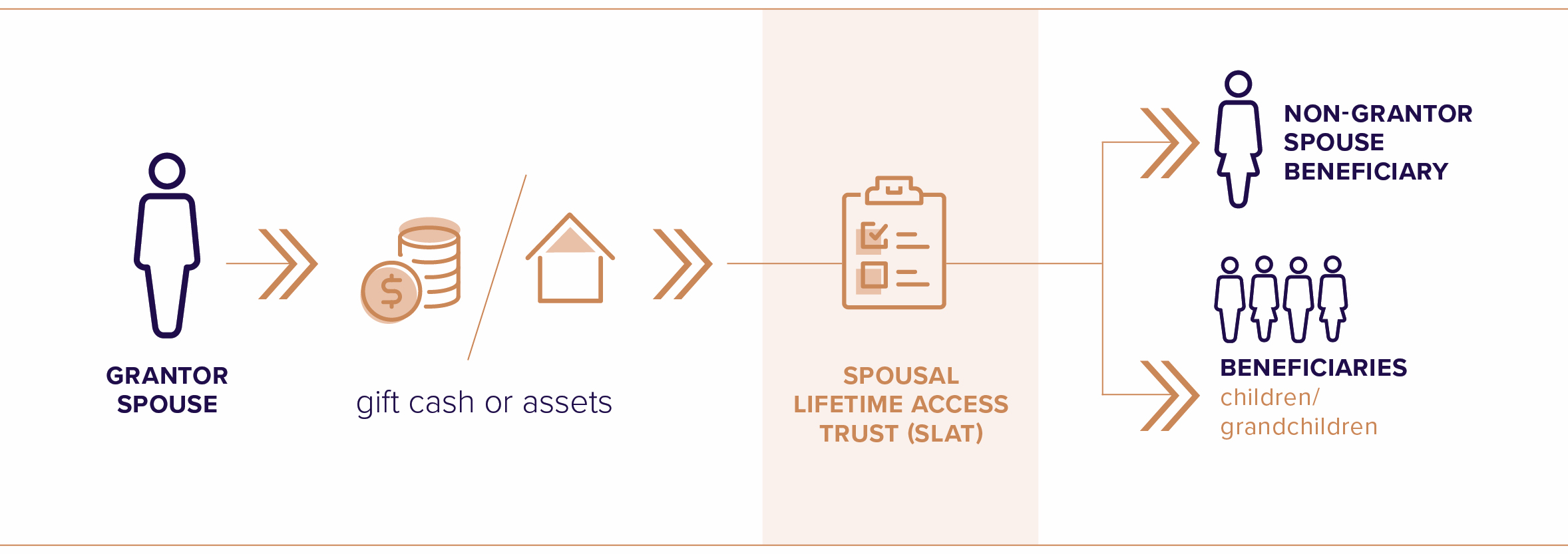

Spousal Lifetime Access Trusts (SLAT)

A Spousal Lifetime Access Trust, commonly referred to as SLAT, is a wealth transfer planning vehicle designed to utilize a portion of a donor spouse’s lifetime exemption through a gift to a trust for the benefit of their spouse and possible descendants. Once the assets are gifted to the SLAT, they are outside of the taxable estate of both the donor spouse and beneficiary spouse.

Furthermore, the donor spouse will have effectively utilized a portion of (or all) their lifetime exclusion amount. Once the SLAT is in place, the beneficiary spouse (and possibly the couple’s descendants) can benefit from distributions of principal and income from the trust—both on a standard basis (i.e., required income distributions) or flexible discretionary basis depending on the desired outcome of the wealth transfer planning strategy.

Since the distributions are going to the donor’s spouse and children, the family unit does not see a significant impact on their cashflow after implementing the SLAT. It is for this reason that many VHNW families have incorporated SLATs into their pre-sunset estate planning. In particular, if both spouses engage in such planning (being careful of reciprocal trust problems), it is possible that VHNW families can utilize a substantial portion, if not all, of their pre-sunset exemption levels. However, SLATs are not without risk and nuances to their effectiveness, which are explored in more detail in my previous Insight on SLATs found here.

Domestic Asset Protection Trusts (DAPT)

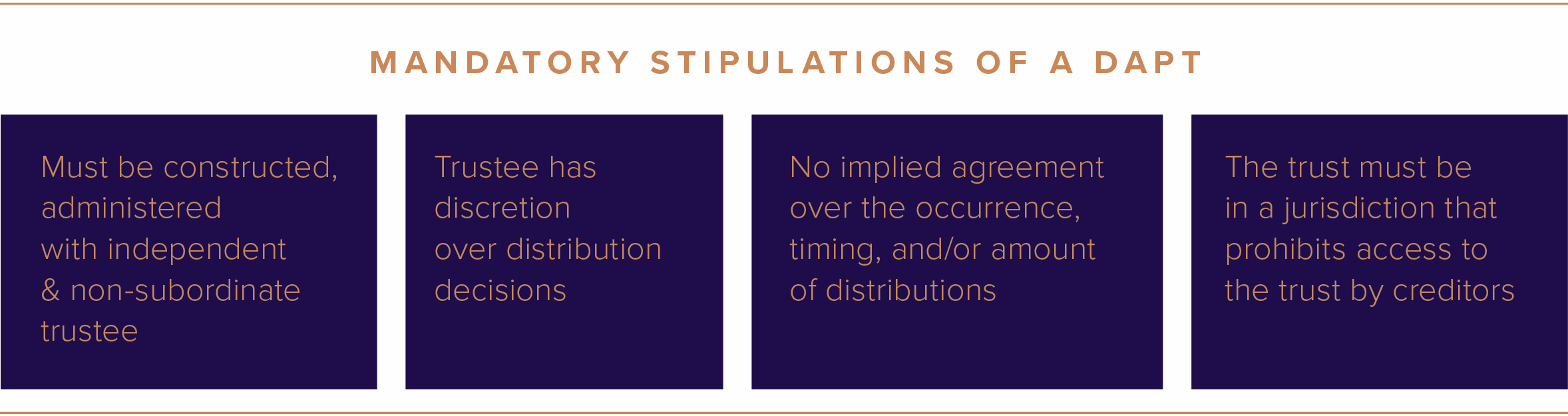

A Domestic Asset Protection Trust, commonly referred to as a DAPT, is a self-settled trust established in a favorable state jurisdiction where the settlor’s creditors do not have access to the assets of the trust, and the settlor also retains a carefully constructed and non-pervasive beneficial interest in the trust. While DAPTs have long been used for asset protection purposes, particularly by those in high-risk occupations, their use as planning vehicles to utilize a portion of the estate tax exemption before the sunset is a relatively novel approach. To be a completed gift, and thus utilize a portion of the taxpayers lifetime exclusion amount, a DAPT must be constructed and administered where there is a completely independent and non-subordinate trustee in place that has discretion over distribution decisions to the beneficiary. There also cannot be an implied agreement over the occurrence, timing and amount of distributions between the trustee and beneficiary. Finally, it is essential that the trust has situs in a jurisdiction that sufficiently prohibits access to the trust principal by creditors.

DAPTs can be an effective planning vehicle to utilize a substantial portion of the settlor’s lifetime exemption. However, given the constraints around access to trust principal and the expectation of distributions, they are likely not appropriate vehicles for a majority of someone’s assets. That being said, they have the ability to be powerful tools when used in conjunction with other planning strategies to “push you over the edge” to save estate taxes in certain planning circumstances.

Qualified Personal Residence Trust (QPRT)

QPRTs have been a mainstay in estate planning for a long time. They are an irrevocable trust that is established to transfer a primary or secondary residence out of a homeowner’s estate, while retaining an interest in occupying the residence, rent free, for a predetermined period of time. When transferring the property into the trust, the homeowner utilizes a portion of their lifetime exemption, determined by the FMV of the property, any applicable discounts based on ownership or control and the appraised value of their retained right of enjoyment. After the term of retained use expires, the residence and any appreciation since the initial transfer is out of the previous homeowner’s taxable estate. If the original homeowner does not survive the term of the QPRT, the value of the gift and any subsequent appreciation reverts back to being included in their taxable estate. As such, the QPRT term is a key variable in determining the value of the gift and the effectiveness of the planning technique. Various strategies can be used to mitigate some of this risk, such as transferring multiple interest percentages at different times to multiple QPRTs.

Since a QPRT generally allows the homeowner to continue to enjoy and control the property for a predetermined period of time and utilizes a generally illiquid asset in their estate, they can be ideal planning vehicles for VHNW families who want to incorporate a strategy to employ a portion of their lifetime exemption that may otherwise be reduced after the sunset at the end of 2025. Additionally, at the termination of their right to enjoy the property, they may be at a point in their life where they are more accepting of dwindling their taxable estate by paying FMV rent to continue to enjoy the residence, especially if their estate is even more taxable at that point in time.

Traditional Trusts for Children & Grandchildren

While there is nothing special about traditional trusts for children and grandchildren from a pre-sunset estate planning perspective, their usefulness in coordinated planning to take advantage of the current high exemption levels should not be overlooked. Using a portion of a taxpayer’s lifetime exemption to fund a trust for their children or grandchildren may seem counter-intuitive to the theme of this article, which is planning techniques that potentially save estate taxes while limiting the impact on their current spending and lifestyle. However, part of the spending patterns and financial cost for many wealthy individuals includes the support of their children and grandchildren to some degree. To the extent that the taxpayer has the desire to continue this support for the foreseeable future, formalizing it through the use of a traditional trust structure may accomplish their goals, while leveraging a portion of their lifetime exemption amount that would otherwise be lost after the sunset. It is unlikely that this would be the only strategy deployed in the effort to leverage a portion of their lifetime exemption that may otherwise be lost post-sunset, but when used in conjunction with other planning vehicles or previously deployed planning, it may be an effective approach.

Uncertainty in the estate planning environment is nothing new, and practitioners are constantly balancing current rules with prospective legislative changes and threats of systemic overhauls from Congress. In approaching planning, wealthy taxpayers, particularly those caught in the middle, need to have a clear understanding of their tax exposure in the most likely scenarios, a firm understanding of their personal goals and objectives, and the degree of impact on their personal lifestyle they are willing to accept in any planning strategies. Once those things are clear, collaboration with their estate planning team can produce effective solutions. Planning strategies like those discussed above can help mitigate the risk of implementing a plan that the taxpayer may later regret.