It’s hard to believe that it’s only been two months since the COVID-19 pandemic took grip of the US health system and economy. We’re in a vastly different world today than the last time I wrote several weeks ago. The coronavirus’s impact on millions of lives—those infected and their loved ones—is tragic. The loss of life from this silent foe has now nearly doubled the total American deaths during the Vietnam War. In addition, the loss of time with loved ones has and will continue to cause immeasurable amounts of emotional pain and suffering.

Thankfully, we’re beginning to see a glimmer of light at the end of the tunnel. The number of recovered cases continues to rise. Treatment practices have improved as we learn more about the virus, shortening the length of the average hospital stay and keeping ICU utilization down so that our hospitals are not overwhelmed. Some areas of the country are beginning to phase re-openings and relaxing stay-at-home orders.

After 10 weeks of social distancing and isolation, the desire to get back to “normal” life is understandable. At the same time, however, we still have a long way to go and must remain vigilant in our efforts to decrease the spread and infection rates.

Economic fallout.

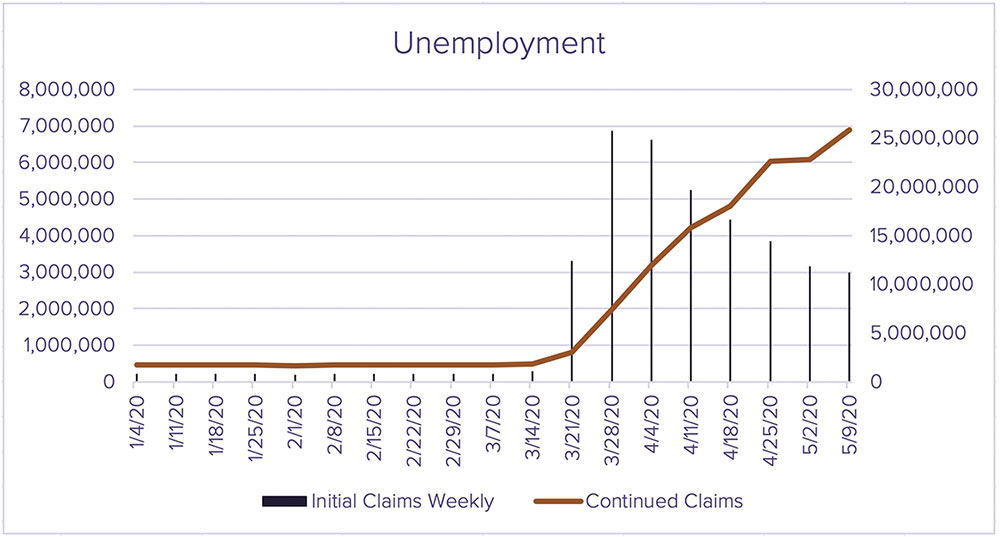

Millions more have had their lives turned upside down by the economic fallout of a halted economy. Unemployment figures have soared to heights we’ve never considered.

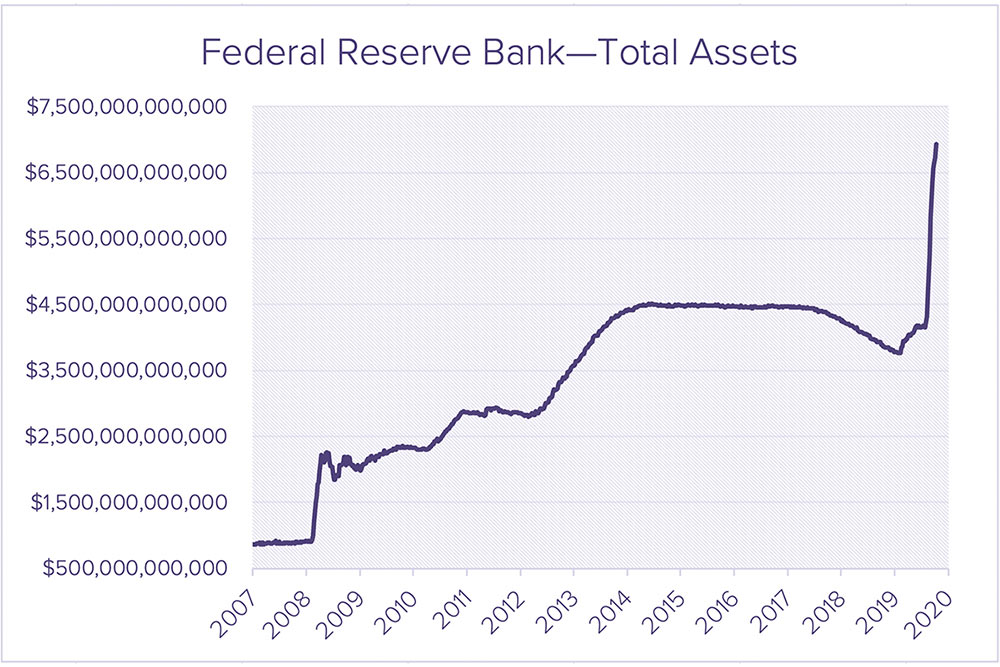

The governments and central banks have done—and will continue to do—what they can to ease this burden on the country and the rest of the world. It took only a matter of weeks for Washington to agree on the CARES Act. The Federal Reserve bank acted even quicker, increasing its balance sheet to nearly double from last fall.

The fiscal stimulus and liquidity injection by the Federal Reserve should set the economy up for a speedy economic recovery when the country and all industries can open for business. The increased money supply and ballooning national debt are certainly concerning from a long-term perspective, but that’s a battle for another day—perhaps even decade or generation.

A generation-defining event.

Speaking of generations, it’s going to be interesting to see the long-term cultural effects of the crisis. Just as 9/11 is the defining characteristic of the millennial generation, this pandemic may be that milepost for Gen Z and the generation that follows.

I’m especially cognizant of this as I spend more time at home with my five-year-old son, Jackson, who quickly added “coronavirus” to his vocabulary and is making fabulous plans for an “everyone-can-get-together party when this is all over.”

Just down the hall from Jackson is our eight-month-old daughter, Felicity. She’ll never know the world that existed before this virus, and I’m endlessly curious about her life experience. Will plexiglass barriers in public be temporary or the new normal? Will our sustainability efforts permanently take a back seat to disposable items? Or, will technology, medicine, and human ingenuity provide a solution to this virus and have us more prepared for the next one? I hope so.

Examining the portfolio.

If you said before this crisis that unemployment would soar past 30 million (>20%); GDP would drop 25% annualized in a matter of weeks; our airports, hotels, and attractions would be empty for months; and that we can’t freely shop, dine, or socialize—yet the S&P 500 would only be down 10%, most reasonable people would say that scenario is impossible. But that’s the truth today.

The constituents of the index certainly tell a more detailed story. Some of the largest technology companies are positive during this time. Consumers are spending more time (and money) in the digital world, now that it’s difficult to spend it in the physical world.

On the other hand, hospitality, tourism, travel, oil and gas, and many other industries are facing unprecedented challenges with demand dropping to near zero. The companies in those industries are suffering, and we’re beginning to hear of some solvency concerns. My colleague, Phil Frattali, dives into more detail on the disparate results across American industries and companies in his article, The Great Bifurcation.

What do we make of this new reality? We have some concerns. A recent article in The Economist, “The market v the real economy” (free with account sign-up), outlines the concerns about the US market far outpacing the underlying economy. The first that we’re aware of is an aftershock of the virus that further disrupts the global economy. Secondly, much like the 2001 and 2008 crises, we could see corporate fraud uncovered, causing investors to lose confidence in the markets. Lastly, the crisis may result in a political response, pushing corporate tax rates back toward their long-term average of 30%, from the current 21%. We could perhaps see a more challenging environment for mergers, acquisitions, and share buy-backs, which have all helped the markets hit their lofty all-time highs earlier this year. These are all areas that we will continue to monitor.

What we’ve been doing.

While much of the firm has not been in the office over the past few weeks, the Sanderson team has been hard at work collaborating on how to navigate our clients through these unprecedented times. Here is a summary of the strategies and actions we’ve been deploying.

- Throughout the most volatile times of the crisis, we were very active in harvesting tax losses while maintaining market exposure. We’re now past the 31-day wash-sale rules and approaching or past any short-term trading issues, so we’re tuning up our portfolios for the longer-term recovery.

- We’re maintaining or increasing active management as some companies will likely experience solvency issues.

- We’re retooling our non-traditional allocation for the realities of the current market, with an emphasis on decreasing credit risk, rebalancing real estate and infrastructure, and being mindful of the market beta in our alternative strategies section.

- Lastly, we’re raising cash for our clients who are drawing on their portfolios. We want to have 6+ months of draws covered with cash in case the market decides it’s gotten too far ahead of the economy and volatility increases.

The pandemic will continue to be a rapidly-evolving situation. There’s no telling where we will be two months from now. However, you can count on Sanderson to be looking out for your present and future financial wellness. If you have any questions or concerns, please don’t hesitate to reach out to your adviser.