A month ago, it seemed unlikely that high-net-worth taxpayers would face any significant changes to the current historically generous estate, gift and generation skipping transfer tax (GST) regime until the expiration of the Trump-era Tax Cuts and Jobs Act (TCJA) provisions at the end of 2025. The Democratic Party's sweep of the Senate run-off elections in Georgia, however, have rocked the estate tax landscape and made many of the changes proposed by the Biden administration appear to be much more imminent. There has even been talk of making such changes retroactive to the beginning of 2021. While such a dramatic and abrupt retroactive change seems unlikely, changes within 2021 or 2022 are nearly a given with the consolidation of Democratic control. So what should high-net-worth taxpayers expect to see and how can they plan now to avoid the implications of some of these changes?

Significantly Reduced Transfer Tax Exemptions.

The lifetime estate/gift/GST exemption amount for 2021 currently stands unified at $11.7MM per person, with portability of any unused estate tax exemption to a surviving spouse. The Biden administration has indicated that they would like to decrease the estate tax exemption amount to the Obama-era amount of $5MM per person (possibly indexed for inflation to around $6MM), or perhaps even lower to $3.5MM per person. Portability of unused estate tax exemption is likely to remain given its impact on the simplification of estate planning process for many taxpayers.

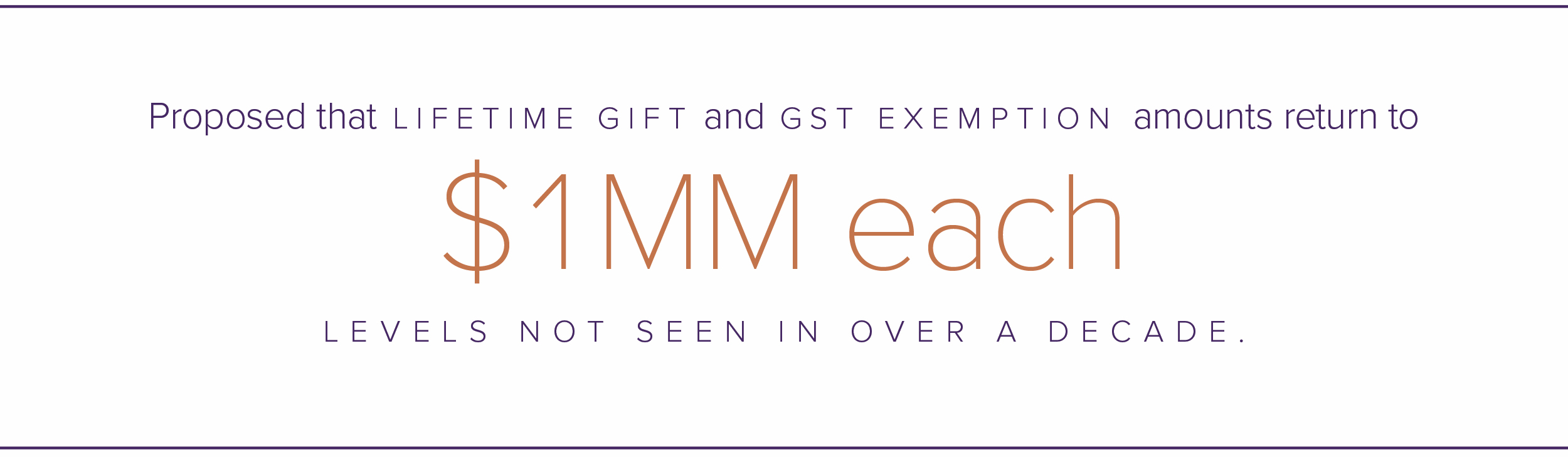

Additionally, it has been proposed that lifetime gift and GST exemption amounts possibly return to $1MM each, levels not seen in over a decade. With such a significant reduction in exemption levels, many more taxpayers will see themselves subject to these transfer taxes, and planning to avoid these taxes will become more challenging and widely important to preserve family wealth for future generations.

Taxation of Unrealized Gains at Death.

A foundation of traditional estate planning has been the consideration of the step-up in basis for appreciated assets includable in the taxpayer’s estate at their death. Currently at death, the fair market value (FMV) of assets are generally includable in the calculation of the applicable estate tax liability for the deceased. Since the assets were subject to the estate tax regime at their FMV, the heirs of the deceased received income tax relief on those assets, as any inherited appreciation generally avoided capital gains taxes in their hands (and in those of the deceased).

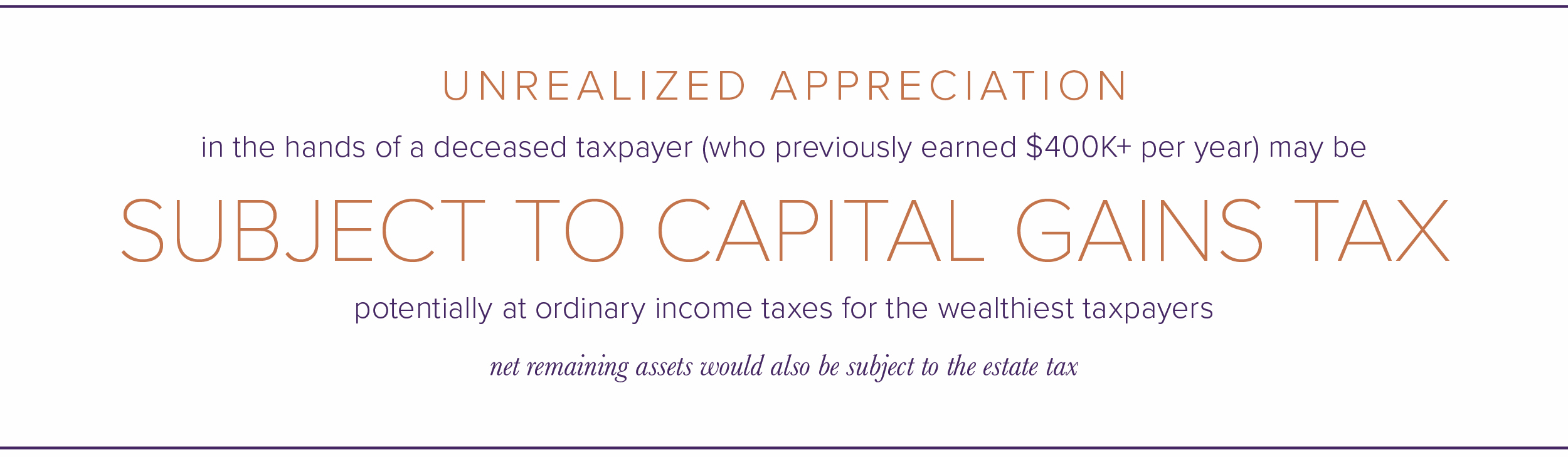

The Biden administration has proposed a significant change to this traditional treatment. Not only would unrealized appreciation in the hands of a deceased taxpayer (who previously earned more than $400K per year) be subject to capital gains tax (potentially at ordinary income taxes for the wealthiest taxpayers), the net remaining assets would also be subject to the estate tax.

This is a significant break from conventional estate tax norms, even during previous Democratic administrations. However, it would generate much more tax revenue than simply reducing the exemption amounts alone. We expect this to be a heavily debated component of Biden’s proposed estate tax reform, with the double taxation being a difficult pill for many moderate Democrats to swallow. However, it is entirely possible that the application of this concept on some level is worked into a compromise when ironing out the specifics of the other proposed estate tax changes.

A softer approach being considered is to not have unrealized gains automatically taxed at the death, but rather eliminate the step-up in basis to date of death FMV for heirs. This would have the impact of shifting the income tax burden on inherited appreciated assets to beneficiaries. However, the next generation would at least have the ability to control the timing of recognizing the capital gains, providing planning opportunities.

Increase in Transfer Tax Rate.

The TCJA maintained the Federal tax rate for estate/gift/GST purposes at 40%. The Biden tax plan looks to increase this rate to 45%. Coupled with the significantly lower exemption and ununified amounts noted above, the administration looks to raise significant tax revenues from high-net-worth individuals with taxable estates. In fact, the combination of a lower exemption amount, increased estate tax rate, and a capital gains tax on unrealized appreciation at death could yield an effective “death tax” rate of over 67% on heavily appreciated assets for very large estates.

Probability & Timing of Changes.

With the Democrats having consolidated control of the White House and Congress, the passage of estate tax legislation over the next year seems much more probable. However, the slim margin by which they maintain Congressional control may moderate their approach, both in respect to the scope and timing of it.

While members on the extreme left will be in favor of implementing the most punitive versions of the changes noted above, many analysts believe that more center-leaning Democrats and Biden’s desire to reach across the aisle to some extent will cause the final changes to be more moderate, increasing the likelihood of prompt passage.

Additionally, while there has been some chatter about making any changes retroactive to January 1, 2021, with the same desire and need for moderation, it is more likely that any changes will be prospective to the new 2022 calendar year, or at the very least not retroactive to the beginning of 2021. The continued focus on controlling the Covid-19 pandemic and dealing with the present economic fallout from it further strengthens the argument for not seeing estate tax changes until 2022 as well.

While estate taxes are certainly a hot button issue that typically increases partisan divides, it’s actually not a significant source of tax revenue for the U.S. (try telling that to the taxpayers paying it!). With so many more pressing issues on the Congressional stove in this transition year, we agree that it is less likely that we will see any changes enacted for 2021. However, that does not mean there is no need to start planning immediately.

Estate Planning Considerations to Start Thinking About Now.

The window for planning under the current generous estate tax landscape is open now. While there is some risk to enacting transfers today if enactment is retroactive, it can generally be mitigated somewhat through creative estate plan and trust drafting techniques.

The most obvious and impactful planning idea today is to make use of the current lifetime gift and GST exemption levels before they are essentially gone. The current gift/GST exemption amounts are $11.7MM per person, which could be reduced to $1MM per person. However, it is important to note that lifetime gifting accumulates from the bottom up, so to make use of the entire exemption amount today, a gift of $11.7MM would need to be made, not just the difference between the current exemption amount and the proposed new $1MM or $5MM exemption levels. For many moderately high-net-worth families (say $10MM to $50MM estates), this may be impractical.

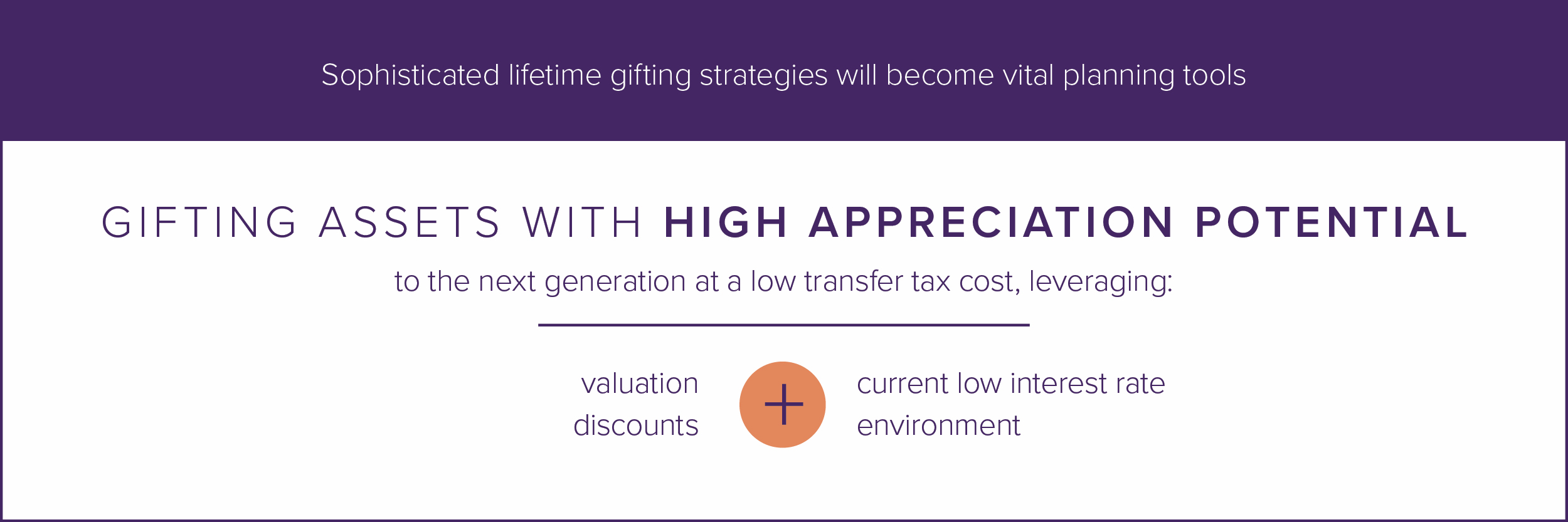

For those who can afford to make substantial gifts to the next generation and for those who will be forced to enact their planning under the eventual new rules, sophisticated lifetime gifting strategies will become vital planning tools. These strategies will center around gifting assets with high appreciation potential to the next generation at a low transfer tax cost (i.e., use of lifetime exemption amounts) by leveraging valuation discounts and the current low interest rate environment. Grantor retained annuity trusts (GRATs), charitable lead annuity trusts (CLATs) and intentionally defective grantor trusts (IDGTs) will continue to be popular vehicles to avoid estate taxes and become critical planning tools for a wider base of taxpayers.

Some of the planning vehicles themselves, and components thereof (such as valuation discounts), will be under scrutiny by the new Biden administration. It is possible that we will see the effectiveness of these strategies diminished by legislation as well, thus dwindling the estate planning toolkit.

As the details of the eventual new estate tax legislation is unveiled, other estate planning techniques will inevitably emerge. The potential for significant changes to income taxes, coupled with the capital gains tax on unrealized appreciation at death for some, comprehensive planning will weigh income tax and transfer tax considerations against each other, and the results will be a critical component when evaluating the effectiveness of the overall estate plan.

A word of caution.

History has shown us that no tax law is forever. While your planning needs may seem critical under the proposed estate tax changes, causing you a feeling a haste, most effective gifting strategies are irrevocable and carry with them a loss of control. The permanency of these strategies must be weighed against your lifestyle and time horizon when considering their use. We will see generous estate tax exemptions again in the future, perhaps even periodic repeals, along with periods of tightening rules as are on the horizon. All of these factors must be thoroughly discussed and evaluated to avoid a feeling a “buyer’s remorse” and to enact an estate plan that fits a family for generations.