The massive year-end $1.7 trillion budget that President Biden signed into law on December 23, 2022 included more than just the late annual US government budget. It also has most of the components of a retirement savings bill dubbed SECURE 2.0 Act (Setting Every Community Up for Retirement Enhancement) that passed the House earlier this year, as well as some provisions from the Senate’s EARN Act. Both bills had overwhelming support, yet neither was moving forward on its own, so Congress combined them into the must-pass omnibus budget bill. There are more than 100 retirement provisions within the SECURE 2.0 Act, but the following are some key provisions:

Increased age for Required Minimum Distributions (RMDs).

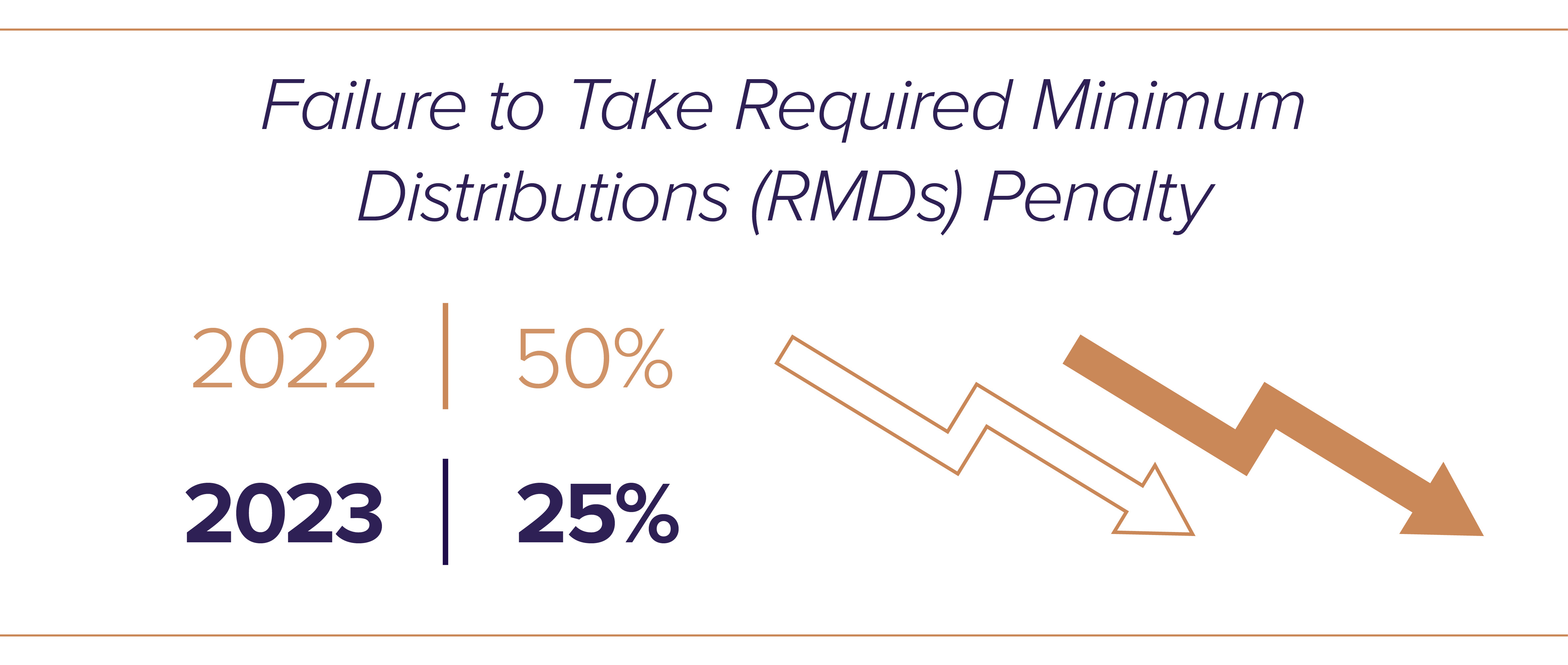

The SECURE 2.0 Act raises the RMD from age 72 to 73 beginning January 1, 2023 (those who turned age 72 in 2023 have one additional year to delay taking RMDs), then age 74 beginning January 1, 2029, and finally age 75 beginning January 1, 2033. As people’s lifespans increase, requiring retirement funds to last longer, the provision will push out the starting age for when RMDs begin. The penalty for failing to take your RMD when scheduled is dropping from 50% to 25%. Special provisions apply for employer Roth 401(k) and 403(b) plans and will no longer be subject to the RMD rules starting in 2024.

Mandatory automatic enrollment in new retirement plans.

Beginning in 2025, most new 401(k) and 403(b) plans must automatically enroll participants with a minimum initial 3% deferral and a maximum of 10%. From there, the deferral escalates at 1% per year of service, up to a minimum of 10%, and maximum of 15%. This is intended to increase participation and the amount of funds participants set aside for their own retirement. Participants will then need to opt-out if they do not want to contribute.

Exceptions of this provision are employers with existing plans, small businesses, new businesses, churches, and government plans.

Higher retirement account catch-up contribution limits.

Catch-up contributions to 401(k) and 403(b) plans have been available for those ages 50 and older and are set at $7,500 for 2023. Beginning in 2025, the SECURE 2.0 Act increases those limits for those ages 60–63 to $10,000 and will be indexed for inflation; however, there is one caveat: if you earn more than $145,000 in the prior calendar year, all catch-up contributions at age 50 or older will need to be made to a Roth account (i.e., after-tax dollars). Individuals earning $145,000 or less, adjusted for inflation going forward, will be exempt from the Roth requirement. Catch-up amounts for IRAs will now also be indexed for inflation after 2023.

Matching for Roths.

Employers will now be able to provide employees with the option of receiving vested matching employer contributions to Roth accounts, although it may take some time for plan providers and payroll systems to adopt this change. Previously, matching in employer-sponsored plans was only done on a pre-tax basis. Employers would still be able to take the deduction for employer Roth matching contributions, but it would be a taxable benefit to participants who elect this Roth matching. Those currently in a lower tax bracket than where they expect to be during retirement, or who have many years for the Roth account to compound may benefit from the tax-free withdrawals that the Roth option offers.

Saver's match.

The non-refundable saver’s credit for retirement contributions will be replaced in 2027 with a federal matching contribution that will be deposited directly into your IRA or retirement plan. The match will be 50% of the IRA or retirement plan contributions of up to $2,000 per person, subject to income limits and phase-outs. This will help boost the retirement savings for nearly 108 million eligible Americans.

Employer fund match for student loan payments.

Beginning in 2024, employers will be allowed to make a matching contribution to participants’ retirement plans based on student loan payment amounts for any loan taken out for higher education. This is intended to assist those with such large student loan balances that they sacrifice their retirement savings. So instead of an employer just matching participant deferrals, in essence they can count student loan payments as if they were retirement deferrals for purposes of retirement plan matching.

Hardship withdrawals.

Participants can withdraw up to $22,000 to pay for expenses related to a natural disaster, which would be taxed as gross income over three years without additional penalty. Survivors of domestic abuse could also withdraw the lesser of $10,000 or 50% of their retirement account without penalty upon self-certifying as a survivor of domestic abuse.

Retirement savings "lost and found."

The SECURE 2.0 Act will create a searchable database to help people locate retirement plan balances that they have lost track of—which is not uncommon when employers change names, merge with other companies, or change plan providers. Also, to reduce the number of old employer plans, it permits retirement plan service providers to offer sponsors automatic portability services, transferring an employee’s low-balance retirement account to a new plan when the employee changes jobs. This would also help limit employees cashing out their plans when they leave their job, resulting in them having to pay taxes and possible penalties.

College savings account rollover.

Leftover 529 account savings could be rolled over into a Roth IRA for the beneficiary without penalty, provided the rollover amounts fall within the usual annual contribution limits, and the 529 plan is at least 15 years old. This provision is subjected to an aggregate lifetime limit of $35,000.

Qualified charitable distributions (QCDs).

Beginning in 2023, people aged 70 ½ and older may elect their QCD limit as a one-time gift of up to $50,000—adjusted annually for inflation—to a charitable remainder unitrust, a charitable remainder annuity trust, or a charitable gift annuity. This is an expansion of the type of charity or charities that can receive a QCD. This amount counts toward the annual RMD, if applicable.

Note: For the gift to count, it must come directly from your IRA by the end of the calendar year.

Next steps regarding the SECURE 2.0 Act.

When reviewing the Act as a whole, the provisions are plentiful; however, it’s crucial to understand the recent changes and how they may impact your retirement planning and wealth strategy. As always, the updated Act is available online and viewable through the Senate’s government website.

For peace of mind and to ensure you’re reaping the full benefits of the SECURE 2.0 Act, reach out to your adviser or contact Sanderson for a consultation.