For many of our clients, philanthropy and giving back is a cornerstone of their family’s foundational values and beliefs. Regardless of a person’s level of wealth, contributing time, money, and resources to a charitable cause near and dear to their heart can be immeasurably rewarding.

The Tax Cuts and Jobs Act of 2017 (TCJA) has significantly altered the standard deduction amounts for individual taxpayers, as well as certain itemized deductions. These changes will likely result in far fewer people itemizing their deductions than in the past. As a consequence, it may also cause taxpayers to unknowingly miss out on receiving a tax benefit from their charitable contributions.

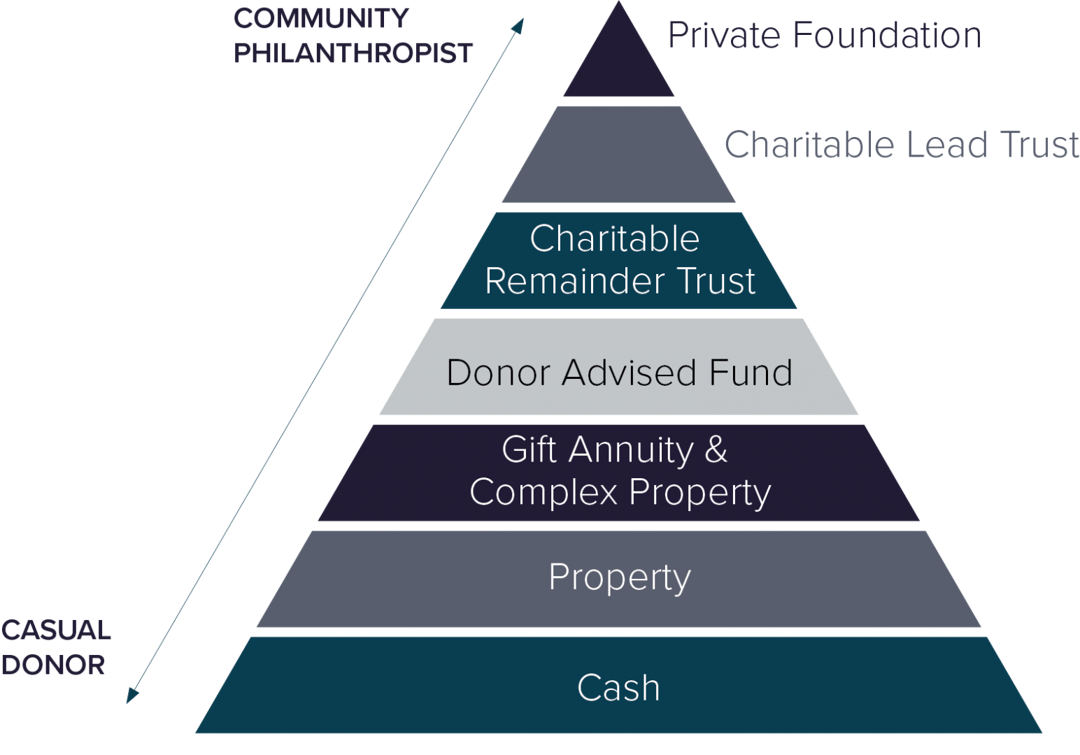

Fortunately, there are income tax planning strategies to help most people manage their charitable contributions in order to achieve the maximum tax deduction for them. For a majority of our clients, annual strategies such as Itemized Deduction Bunching and the use of Qualified Charitable Distributions (QCD) from IRAs will be very beneficial and sufficient. Wealthy individuals and those with longer-term philanthropic legacy goals, along with sufficient financial resources, may find themselves more aligned with philanthropic planning vehicles such as donor advised funds (DAF) and private family foundations. Charitable trusts may also help these individuals balance securing their charitable legacy with meeting their family wealth aspirations.

Annual charitable planning strategies.

In reaction to the changes in the tax law, there are two primary strategies many taxpayers will find useful. Let’s examine both.

- “Itemized Deduction Bunching” (IDB) centers around timing expenditures for deductions such as medical expenses, tax payments, and charitable contributions into a single year, so when combined, they far exceed the standard deduction amount. As such, in years where the standard deduction is claimed, those itemized deductions aren’t “lost” under the standard deduction threshold amount. This combination of isolating between taking the standard and itemized deductions maximizes the tax benefit realized from each category. Using a donor advised fund, which we will discuss momentarily, can assist in the execution of this planning strategy.

- Qualified Charitable Distributions (QCD) are distributions of up to $100,000 made to qualified charitable organizations directly from an IRA by taxpayers who are in RMD status (over age 70 ½). While these contributions can’t be claimed as itemized deductions, the QCD amount from your IRA is not included in gross income as a typical RMD or IRA withdrawal would be. However, the distribution still qualifies for fulfillment of your required minimum distribution for the year. As such, the taxpayer essentially receives an “above-the-line” charitable deduction for the QCD amount as it lowers the taxpayer’s adjusted gross income without having to itemize its deductions. Furthermore, keeping the taxpayer's adjusted gross income down may be helpful for determining eligibility for a variety of other deductions and tax credits.

Creating a legacy with a Donor Advised Fund or private foundations.

Donor advised funds (DAF) and private non-operating foundations are both charitable planning vehicles that enable families to secure a long-term philanthropic legacy. People typically fund either of these vehicles in a year where they are engaged in an itemized deduction bunching strategy, or in a year that corresponds to a significant income recognition event or unusually high earnings (thus maximizing tax savings at a relatively high marginal tax rate). In both cases, the taxpayer receives a tax deduction in the year of funding the vehicle, subject to the following limitations.

| Donation of Cash AGI Limitations |

Donation of Appreciated Securities AGI Limitations |

|

|---|---|---|

| Donor Advised Fund | 60% | 30% |

| Private Foundation | 30% | 20% |

When evaluating the use of any charitable planning vehicle, taxpayers must keep these limitations in mind, along with the 5-year carryforward period to use any disallowed donations.

Once funded, the donor can use either vehicle to direct gifts to the qualified charitable organizations of their choosing in subsequent years.

Despite the initial similarities between DAFs and private non-operating foundations, they become very different over the remainder of their lifespan, both administratively and functionally. The table below highlights the significant administrative differences.

| Donor Advised Funds | Private Foundations | |

|---|---|---|

| Initial Set Up Costs (est.) | TBD | $5,000 to $7,500 |

| Accounting Ongoing Maintenance | Sponsoring charity responsible | Foundation board responsible |

| Annual Accounting Maintenance Cost (est.) | 60 - 15 bps (tiered based on AUM) | $1,000 - $2,000 accounting |

| Income Tax Ongoing Maintenance | Sponsoring charity responsible | Annual 990-PF filing IRS Annual state filings |

| Federal Income Taxes | None | 1% to 2% annually |

| Investment Management | Sponsoring charity generally responsible Independent investment management fees vary |

Foundation board responsible 50 - 100 bps investment management |

| Annual Distribution Requirements | Not required Donor recommends grants |

5% per year required Foundation board directs |

Functionally, donor advised funds and private foundations are different as well. While DAFs provide the donor with some element of recognition on a year-to-year basis (as they direct grants to their favorite charities), they still tend to be vehicles geared toward income tax efficiency rather than toward achieving a long-term philanthropic legacy for the donor and their family.

Private foundations enable donors and their family to become much more engaged in the management and deployment of the family foundation’s resources. This gives the original donor the opportunity to teach their children and future generations about the importance of philanthropy and giving back. While we have all heard horror stories of how substantial wealth has destroyed some family relationships and personal ambition, a family foundation can serve as a platform to promote family interaction, harmony, and a sense of altruism and purpose for future generations whose financial security is already in place. This is often at the core of why our clients decide to set up family foundations.

Private foundations can exist in perpetuity, providing the founder with a recognized legacy in their community, with the organizations and causes near and dear to their heart, and with their families, whose children, grandchildren and generations beyond will forever have a connection to the past, and hopefully an understanding and appreciation for where they are today.

Benefits of a charitable trust.

Where basic annual charitable tax planning falls short, and when DAFs and private foundations don’t quite fit in, or perhaps in conjunction with all of these, charitable trusts may be the right planning vehicle for both lifetime charitable planning and an element of philanthropic legacy planning. While there are many nuanced variations of charitable trusts, the two basic versions are Charitable Lead Trusts (CLT) and Charitable Remainder Trusts (CRT). While these can be set up through testamentary provisions, our focus in this article will be on their use during the lifetime of the trust settlor.

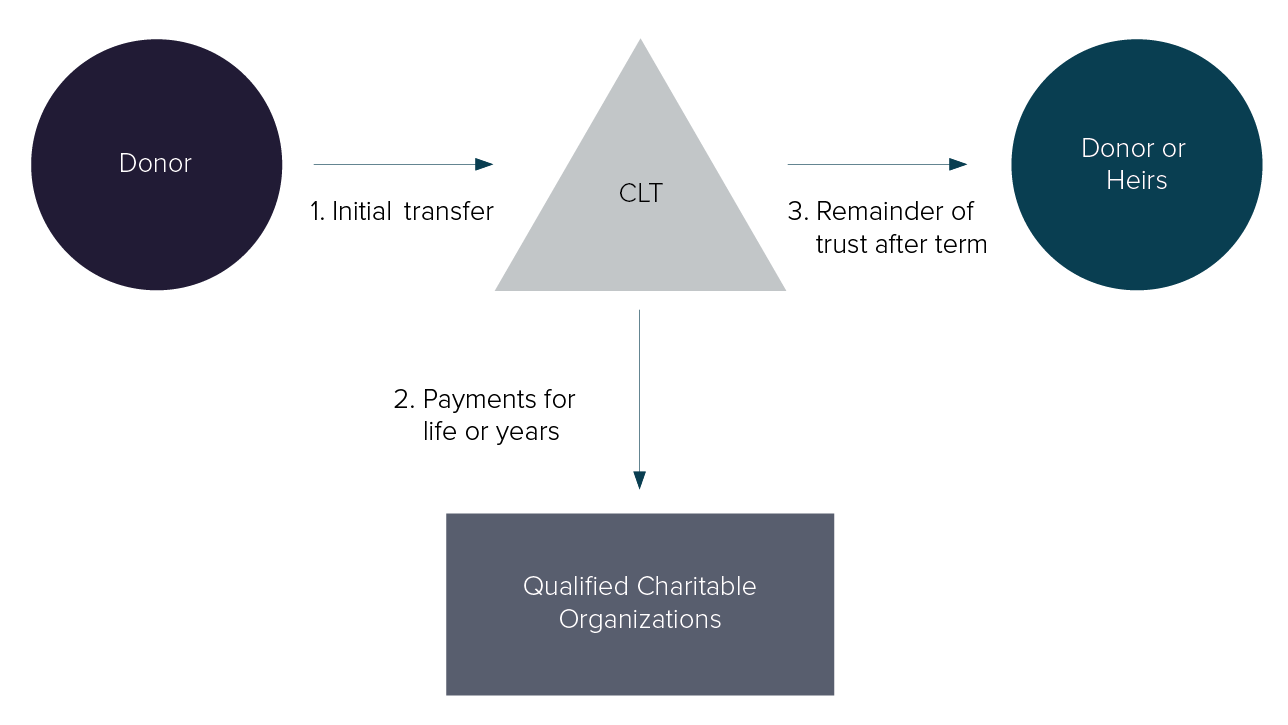

How a Charitable Lead Trust works.

A Charitable Lead Trust is set up to provide a qualified charity with a stream of distributions over a certain number of years, or even the lifetime of the donor or their heirs. At the end of the term, the remaining trust principal is typically distributed to a non-charitable beneficiary, usually a family member in a lower generation. Depending on how the trust is structured, either the donor or the trust itself receives a tax deduction for the actuarial value of the amount benefiting the charity.

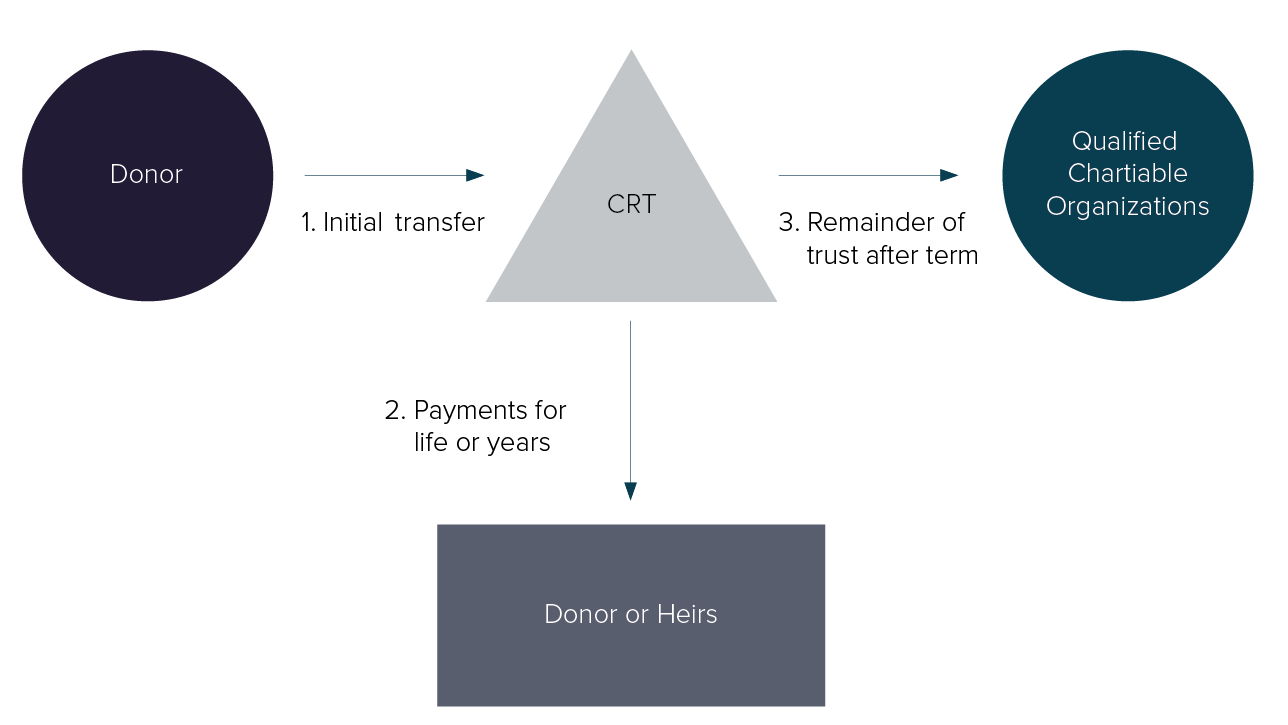

How a Charitable Remainder Trust works.

A Charitable Remainder Trust is usually set up to provide the donor, or perhaps a family member, with a stream of distributions over a certain term or over their lifetime. At the death of the income beneficiaries, the remaining trust corpus is distributed to a designated charity. When properly planned for, these can be very effective vehicles to shelter highly appreciated securities from the initial income tax on capital gains, provide compounded investment return on the tax savings, and enable more efficient income tax management in future years.

When set up during the donor’s lifetime, both CLTs and CRTs can provide the donor with a tax deduction based on the actuarial value of cash flows to charity in conjunction with IRS interest rates in effect at the time (depending on the nature of the trust).

Conversely, this may also yield an estate tax-efficient gift to the family member who is receiving the current income stream or remaining corpus of the charitable trust. Both of these types of charitable trusts can serve as useful planning vehicles for balancing wealth transfers to family and charity. Using charitable trusts, taxpayers can manage the income and estate tax efficiency of their donations, particularly when deployed in coordination with their overall wealth planning strategy.

Summary.

Philanthropy is an important personal and family value to many of our clients. Despite the tax changes caused by the TCJA, robust planning strategies and vehicles still exist to enable clients of all levels of wealth to achieve their charitable goals and aspirations in a tax-efficient manner. Our goal at Sanderson Wealth Management is to guide clients through understanding the various options available to them, and to help them select and place into motion the strategy that best suits the charitable legacy they desire for themselves and the future generations of their family.