How often does the S&P 500 drop 25%?

Between the start of January 2022 and the end of the 3rd quarter, the S&P 500 index officially breached the negative 25% return mark. To understand what historically transpires in this situation, we can look at the data.

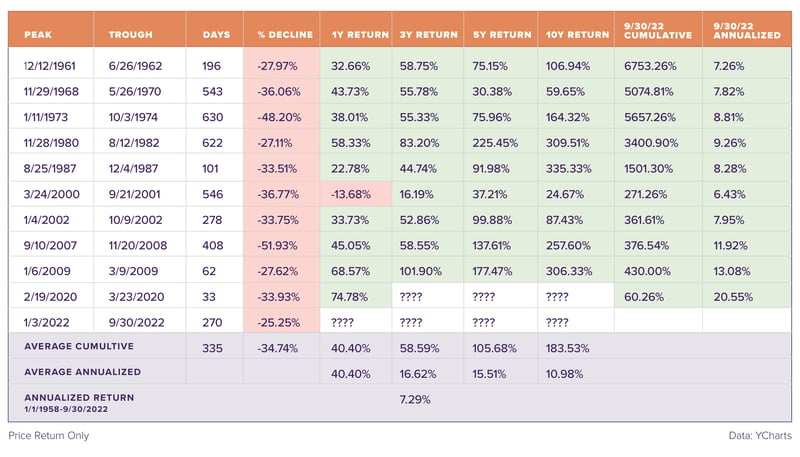

Since the index was introduced in 1957, the S&P 500 has dropped 25% or more 11 times now.

Since the index was introduced in 1957, the S&P 500 has dropped 25% or more 11 times now.

This chart reflects a large variance between the amount of the decline and the length of the decline over the years; however, we are nearing the length of time of an average drawdown. With that being said, the drawdown is not as bad as the average that it usually experiences.

Now, time for some positive news! Obviously, there is a lot of green on that chart. This shows that over short, intermediate, and long-time horizons, you will likely see positive returns after a decline as steep as 25%.

What happens when you invest at the peak?

As some of you may know, market timing is virtually impossible to do, so the above example is theoretical. Here is another theoretical example, what do returns look like if you were to invest at the peak instead of the trough?

.jpg?width=800&height=412&name=chart-2%20(2).jpg)

A takeaway is that although it may take some time, returns eventually turn positive even though they lack the average annualized return of 7.29%. It is virtually impossible to time the exact top of the market just like it is to time the exact bottom. A strategic investor may choose to dollar cost average into the market to avoid trying to time the market; 401k investors will do this naturally over time.

Taking a cue from history.

A standard disclaimer in financial literature is that past performance is not indicative of future results. That is still true, but here at Sanderson, we hope that looking at what has happened historically shows that things typically turn out to be okay for the stock market over the longer term.

Clearly, there are both good and bad times to invest, but we trust that patience, diversification, and timely rebalancing will help our client portfolios experience a smoother ride that is rewarded over the long term.

Past data indicates that much of the worst may be behind us in the markets. We have been through this before at Sanderson, and we will get through this again. This substantial decline in the market does provide an opportunity for new cash to be put to work in the market through investments in stocks, bonds, and non-traditional assets. Please do not hesitate to reach out to us if you have questions or want to discuss any opportunities.