It’s hard to believe, but it’s that time of year again -- when college students pack their bags and return to their dorms, high-school campuses come back to life, and kindergarteners pack their lunch bags for the very first time.

This migration of students back into classrooms is often accompanied by numerous expenses, from costly trips to the bookstore to purchasing the latest laptop computer to choosing the right on-campus residence. According to a 2019 study by Deloitte, the “back to school shopping” industry is estimated to be a whopping $27.8B.

Changes to 529 Plans.

Since their introduction in the mid-‘90s, 529 Plans have been an integral component of saving for qualified college education expenses in an income-tax-efficient manner. More recently, in 2017, the Tax Cuts and Jobs Act heavily expanded the permitted use of 529 Plan funds to include K-12 expenses.

As you swipe your credit card this back-to-school season, please use this chart as a general guide for qualified expenses of 529 Plans. However, keep in mind that some states (i.e., New York) have not conformed to the expanded Federal treatment to include K-12 expenses, thus causing them to be disqualified withdrawals. For clarification, refer to a detailed list of states and their conformity to the TCJA changes to 529 Plans.

| Expense Description | College/Post-Secondary Schools | Grades K-12 (subject to state conformity) |

| Required tuition and fees | Yes | Up to $10K per year, including private schools |

| Books, supplies, and equipment | Yes | Yes |

| Computer equipment & peripherals (i.e., printers) | Yes – primary use college education | Yes – primary use K-12 education |

| On-campus room and board | Yes | Yes |

| Off-campus room and board | Yes – but not exceeding on-campus cost | Yes – but not exceeding on-campus cost |

| Education-related travel | No | No |

| Student loan repayment | No | No |

| Club fees and expenses | No | No |

| College preparatory tests | No | No |

| Expenses for students with special needs | Yes | Yes |

| Trade and vocational schools | Yes – if offered through an eligible institution* | N/A |

| Graduate school programs | Yes | N/A |

| Online colleges | Yes – if offered through an eligible institution* | N/A |

| Adult continuing education | Yes – if offered through an eligible institution* | N/A |

*An eligible institution is one that is eligible for Title IV federal student aid. View eligible institutions, including culinary and cosmetology schools.

529 Plan Rollovers to ABLE Accounts.

One other notable use of 529 Plan funds is the ability to roll balances into an account called Achieving a Better Life Experience (ABLE) for the benefit of qualified disabled individuals. ABLE accounts were introduced in 2014 and allow parents, family, and disabled individuals to save for a myriad of life expenses (particularly ones made more costly and complicated by the presence of a cognitive or physical disability), including education, in a tax-deferred manner.

Often, a child’s disability is not clearly evident until years after saving in a 529 Plan has started. This rollover option provides a great mechanism for saving for the life expenses of a disabled person and balancing the need to save for education expenses for the entire family.

Funding 529 Plans.

The tax-free growth and compounding offered by 529 Plans continue to be a powerful financial planning strategy for saving for qualified college education expenses and, in some instances, K-12 education expenses. Starting to save into 529 Plans for your children or other permissible beneficiaries as early as possible provides the greatest opportunity to defray a portion of the ever-increasing cost of higher education.

Anyone can open a 529 Plan account for a beneficiary. The funding of 529 Plans for family and non-family members is generally subject to traditional gift tax rules. However, there are some unique rules surrounding 529 Plans, which allow gifts in excess of the annual exclusion amount to be averaged over a five-year period (requiring disclosure on a timely filed gift tax return), thus avoiding usage of a portion of an individual’s lifetime estate tax exclusion amount. There are also aggregate limitations on 529 Plan balances, which vary from state to state and range from $235,000 to $529,000. The limitation is based on the expected cost of a beneficiary’s education expenses.

As previously mentioned, wealthy families can consider front-loading five years’ worth of their annual gift tax exclusion into a 529 Plan for each child/beneficiary without using any of their lifetime estate tax exclusion. In 2019, that equates to $75,000 per individual ($150,000 for married couples) into a 529 Plan for a beneficiary!

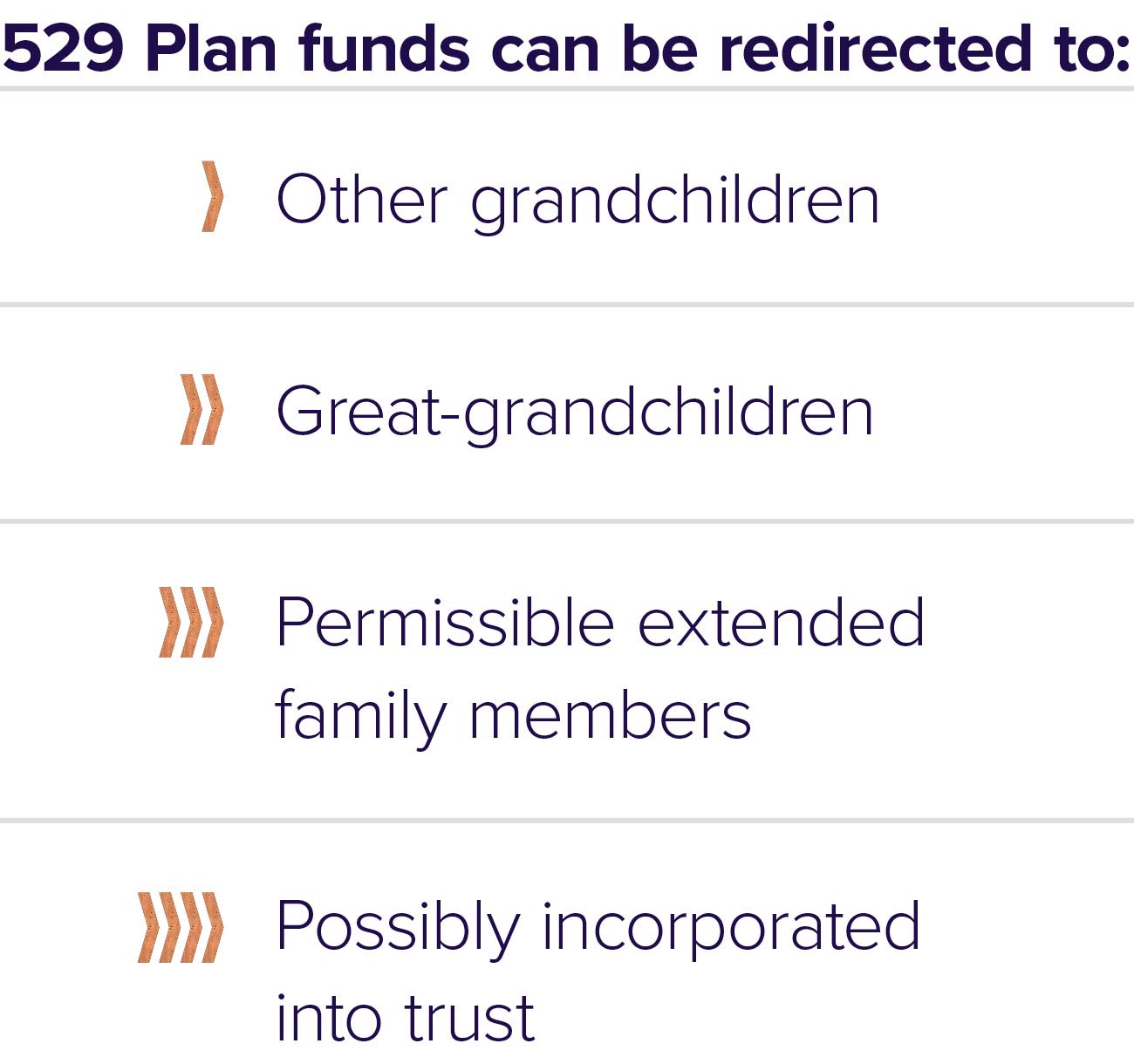

While ultra-high-net-worth families with estate tax exposure will likely want to take advantage of the unlimited gift tax exclusion for college education expenses paid directly to an eligible institution when their children and grandchildren are in their college years, previously funded 529 Plans can be redirected to other grandchildren, great-grandchildren, and permissible extended family members, and possibly incorporated into long-term trust planning instead. This restructuring and redirection of the existing 529 Plans can act as the foundation for a family education legacy, stressing the importance of receiving and leveraging a quality education to future generations.

Conclusion.

Planning around college education expenses can be complicated and nuanced depending on your personal financial situation, especially for wealthy families that have the resources to leverage a variety of planning strategies. At Sanderson Wealth Management, we ensure that, where appropriate, education planning is a key consideration in our client’s overall financial and estate plan.