October brought more tricks than treats to investors this month. Stocks and bonds were both spooked as the Fed-induced bond yield surge continued to weigh on the markets. The Israel-Hamas war also contributed to the risk-off sentiment that shook up the commodity market.

Markets

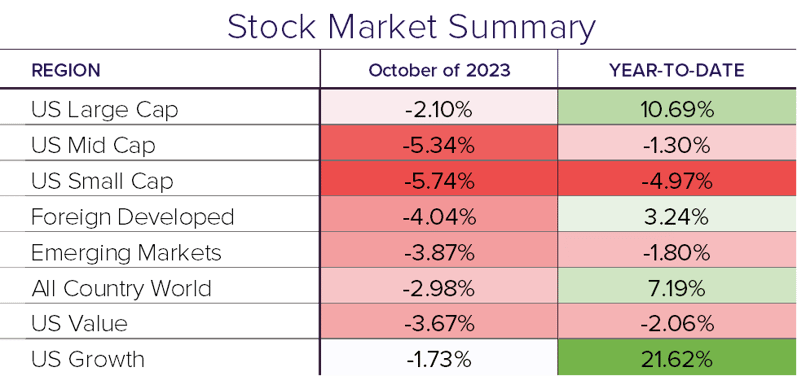

It was a dreary month for the stock market with global stocks down -2.98% in October. Large cap U.S. stocks fared the “best” as they dropped -2.10%, bringing the year-to-date return to 10.69%. Small and mid-cap stocks were both down over 5% in the month, while foreign developed and emerging markets were down -4.04% and -3.87%, respectively. This marks the first 3-month losing streak in stocks since March 2020.

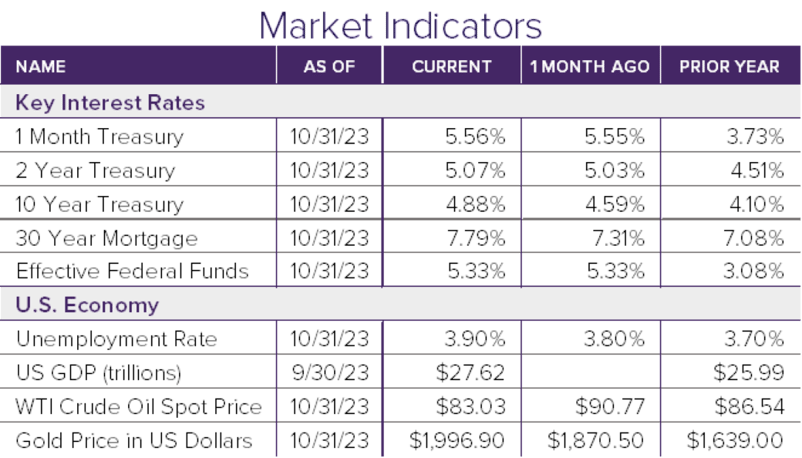

Commodity markets also experienced significant movements. The horrific attacks in Israel led investors to gold which saw its price climb over 6% in the month, briefly topping $2000/oz. Crude oil dropped 8.5% in October after the price hit $90 per barrel in September.

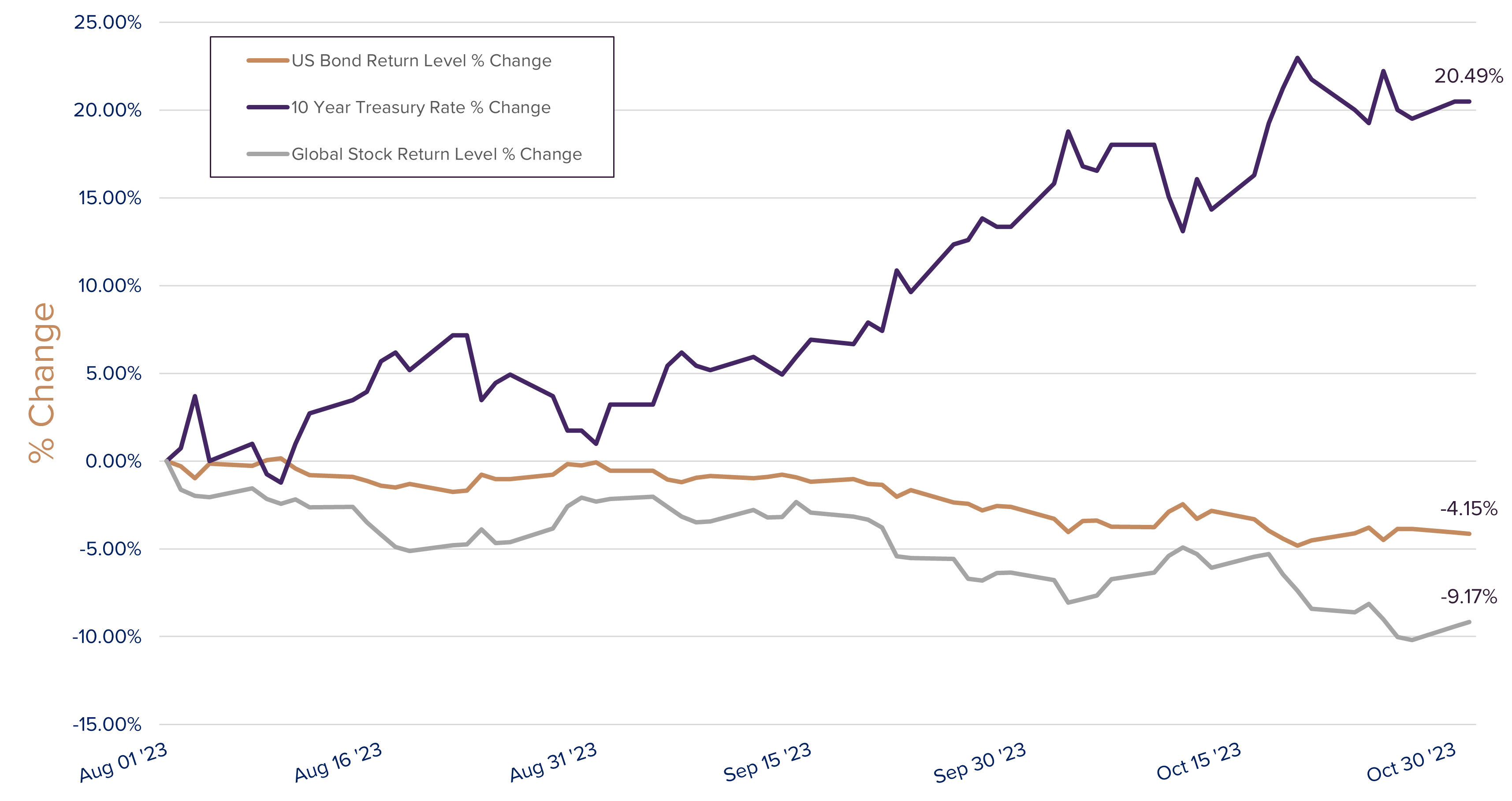

Stocks and commodities weren’t the only markets affected as the U.S. bond market saw prices decline 1.58%. In October, the rate on a 10-year treasury bond went from 4.59% to an intra-month high over 5%, before settling to 4.88%. As a reminder, bond prices move inversely to interest rates. The chart below shows a 20% change, from 4.05% to 4.88%, in the 10-year treasury rate and the resulting effect on the stock and bond markets over the past 3 months.

Interest Rates

This large move in rates comes as the Federal Reserve continues to keep interest rates higher for longer. They have raised rates at the fastest pace in decades, and to a 22-year high to bring inflation under control. Despite not raising rates since July, Fed officials have been unwilling to solidify an end to increases, and even signaled that the next move was more likely to be an increase rather than a cut.

Looking Forward

October was no doubt a scary month for the markets, but the first few days of trading in November are quickly shoving the skeletons back in the closet. Stocks are on pace for a large move higher, and yields have plummeted on the back of soft jobs numbers. If history is any consolation, the S&P 500 has been positive 10 out of the past 11 Novembers.