July certainly did not disappoint. The S&P 500 closed higher for the fifth month in a row. The Dow Jones Industrial Average nearly tied a 126-year-old record for consecutive days of gains, with 13 straight this month. Falling inflation and resilient economic growth encouraged a broad market rally on hopes that the Fed is near the end of its tightening cycle.

Markets

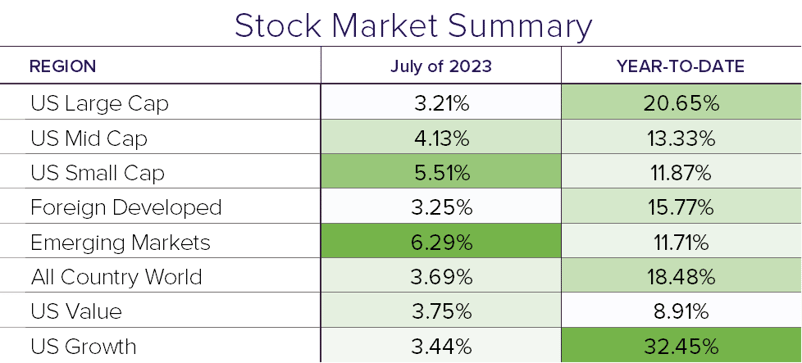

US stocks notched their longest monthly winning streak in two years. The S&P 500 closed 3.2% higher in the month of July, bringing the year-to-date return to 20.1%. Most of that return has been thanks to the Magnificent Seven (Microsoft, Telsa, Nvidia, Apple, Google, Facebook, and Amazon) particularly through the first five months of the year. Over the most recent two months, the market rally has begun to broaden out as the other 493 companies in the index start to catch steam. In fact, an equally weighted version of the index has been up 10.6% since the start of June, compared to the -0.6% return for the first five months of the year.

Elsewhere, we have seen additional strength across the global equity market. For July, mid and small cap stocks were up 4.1% and 5.5%, respectively. Foreign developed markets gained 3.2%, while emerging markets were the standout this month, posting gains of 6.3%.

Economy

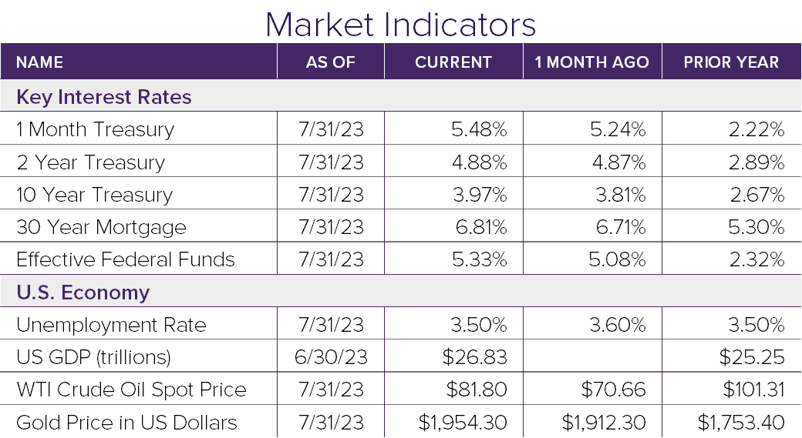

The broadening strength of the market comes as recent economic data suggests the Fed may avoid pushing the US into a recession. In July, the Federal Reserve raised rates another 0.25% to push the Fed Funds target rate to 5.25-5.50%—its highest level in 22 years. The data indicates that the rate hikes are beginning to take effect as inflation (CPI) came in below 3% for the first time in over two years. Core inflation (excluding food and energy) was below 5% for the first time since November 2021. This inflation data came in alongside the GDP report, which showed that the economy grew at a rate of 2.4% year-over-year, beating economists’ forecasts of 1.8%.

Wrap Up

If these trends of slowing inflation and steady growth continue, then the market’s hopes will be validated. If more data comes in suggesting otherwise, then we could see the Fed continue on its path, likely leading to a spike in volatility.