Capital gains rates have been headline news since the change in administration in Washington became imminent one year ago. Often these headlines stir up emotions to sell appreciated assets prior to an anticipated rate hike. This time, like many times before, is different. Investors that volunteered to pay taxes early in 2021 may have moved too quickly as the once imminent capital gains tax-rate hike appears to be dead in the water.

We often find that a knee-jerk reaction to potential new legislation can be damaging and irreversible to a family's wealth. Investors need to consider the bigger picture of lifetime tax burdens, rather than just a year-by-year game against the taxing authorities.

Winning the tax war, not just a battle

Whenever there’s potential for a capital gain tax increase, it’s common for high-net-worth individuals and families to consider unloading highly appreciated assets to avoid the higher rates. However, the decision is not—or shouldn’t be—that simple. We often see clients, especially business owners, maximize deductions to win the year-to-year tax game. Unknowingly, these decisions can hinder their cash flow and long-term wealth.

Regardless of what tax legislation is being proposed (and may or may not be approved), sophisticated planning should take a long-term view that considers the lifetime tax burden, not just annual returns. That may include building a personal balance sheet and paying taxes along the way to avoid a heftier bill in the future.

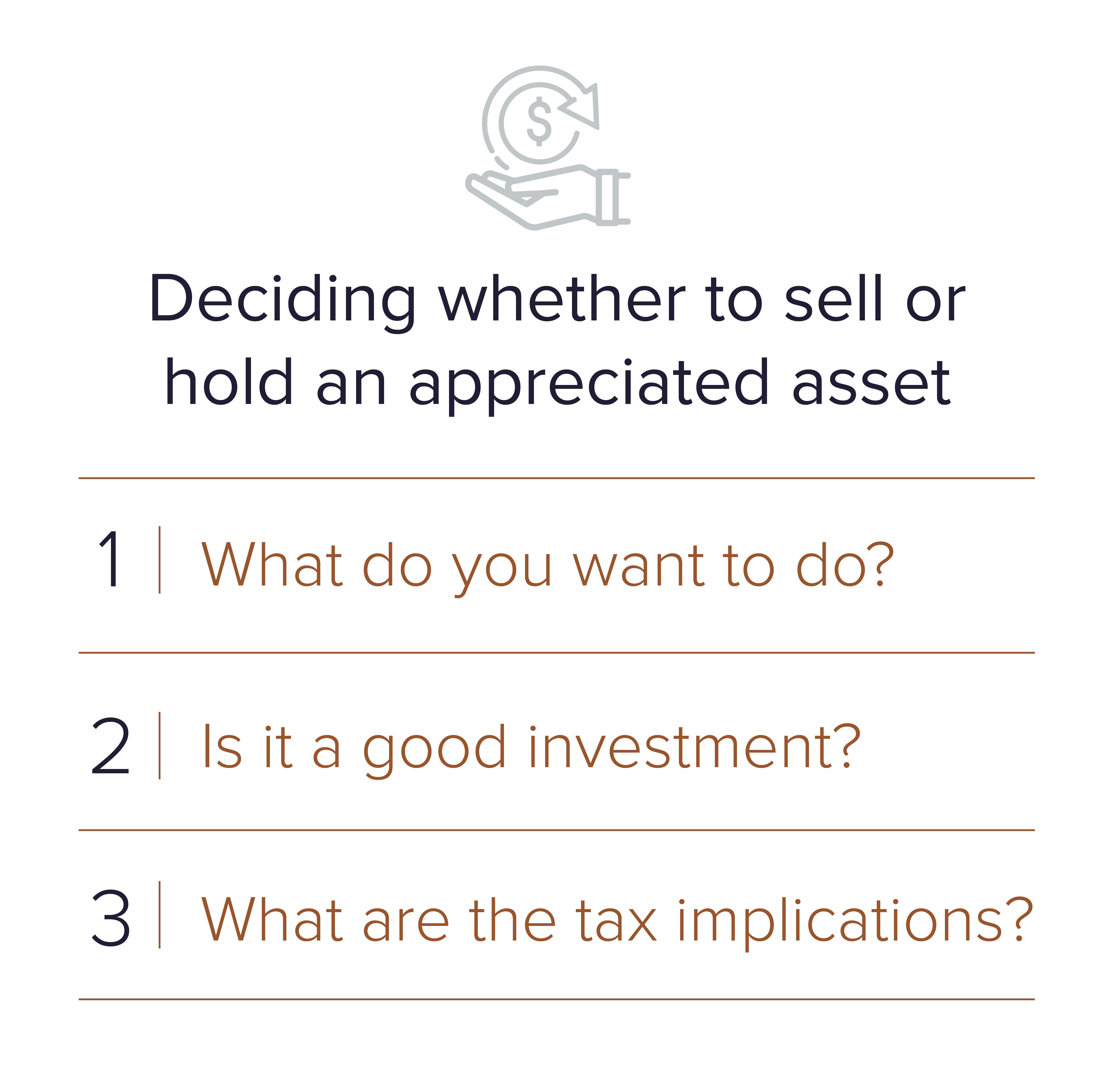

The three big questions

When deciding whether to sell an appreciated asset—such as stocks, real estate, or a business—tax implications should be considered but not be the driving factor. Here are the three big questions, in order of importance, we review with clients in order to land on what makes the most sense:- What do you want to do? Some clients have qualitative reasons or sentimental attachment to an asset, which can be a valid reason to hold on long-term.

- Is it a good investment (regardless of taxes)? This is where quantitative assumptions come into play, including future appreciation and a cost-benefit analysis.

- What are the tax implications? If the first two criteria indicate a desire to sell, we can look for the most efficient opportunities to do so. Timing can be crucial in this regard, such as if you’re experiencing a lower tax bracket during retirement, sabbatical, or another life event.

The final decision often requires a thoughtful conversation with your adviser. Ultimately, we want to evaluate whether the appreciating asset will outperform the eventual tax burden.

When is it wise to sell?

When is it wise to sell?

All of this is not to say that holding on to an investment always delivers the best long-term outcome. There are many situations where selling in the near future could be more advantageous. For example, if a client has a mature portfolio, now may be an opportune time to pay capital gains tax and refresh the basis.

When it comes to assets such as real estate, we urge clients to consider whether they are ready to commit to the investment for the remainder of their life. The reason is that we can minimize the inheritance tax through step-up in basis after death. If that commitment is not desirable, the other option could be to sell the asset, take the short-term tax hit, and put the gains toward an investment that will be better off in the long run.

Wait and see- then act

At Sanderson, we will continue to monitor the progress of the Build Back Better Act. Once we have more clarity on what proposed tax changes will come to fruition, we will inform and advise our clients accordingly. In the meantime, if you have any questions about your assets and potential capital gain tax implications, reach out to your adviser or contact us for a consultation.