Stocks made big moves in February to extend the 4-month rally. A slew of data pointing to a strong economy and labor market coupled with a feverish rally from a handful of growth stocks led to the S&P 500 closing above the 5000 level for the first time. Meanwhile, bond prices fell after hawkish comments from the Fed.

Strong Start

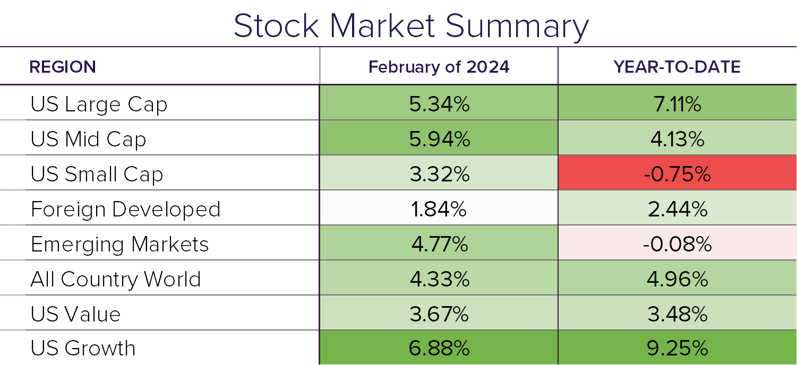

The S&P 500 was up 5.3% in February and 1.7% in January. Historically, this solid performance for the first two months of the year bodes well for the next 10 months. In fact, out of the past 28 times that January and February have been positive for the S&P 500, the final 10 months were positive 26 out of those 28 times. Not only were they positive in those cases, but the returns were better than average.

Driving the strong performance for the large-cap index were a handful of growth stocks. For example, two of the largest holdings in the index, Nvidia and Meta, were up over 25% for the month. Growth stocks in aggregate were up 6.9%, while value stocks finished 3.7% higher. Mid-cap stocks turned positive for the year thanks to the 5.9% monthly return. Globally, emerging markets outpaced foreign developed, returning 4.8% and 1.8%, respectively.

Data Dependency

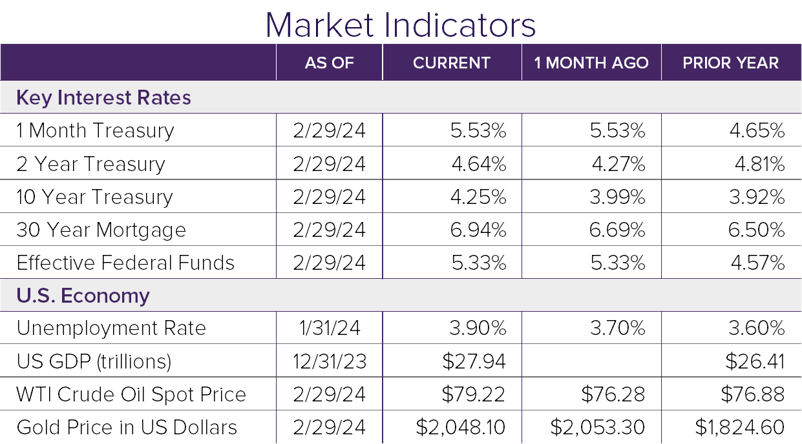

The disinflation trend is still in vogue despite some strong recent data points. The CPI and PPI inflation measurements came in higher than expected, the unemployment rate remained low at 3.7%, and the Fed’s preferred inflation measurement (PCE price index) had its largest monthly increase in over a year. Despite the recent monthly spike, inflation compared to a year ago continues to trend closer to the Fed’s 2% target.

Unsurprisingly, interest rates spiked as rate-cut expectations have been repriced coming out of the January Fed meeting. This led to bonds being down 1.4% for the month.

Looking Ahead

In March, we have Fed chair Powell speaking on Capitol Hill, updated CPI and PPI inflation numbers, and a Fed meeting. Stay tuned!