If we were to rank the top financial topics of 2022, it’s safe to say that interest rates would be toward the top of that list. On March 17, 2022, the Federal Reserve enacted its first increase to the benchmark interest rate as part of its strategy to combat soaring inflation. Since then, there have been a total of six rate increases, each between 0.25 and 0.75%.

For many clients, interest rates can be a somewhat abstract concept. Unless you’re looking to secure a loan or scrutinizing savings account yields, it’s not always apparent how the current interest rate impacts you, directly or indirectly.

Let’s look at who is being affected by higher interest rates and how the Fed’s decisions factor into your overall financial plan.

Home buyers.

For over a decade, homebuyers have enjoyed historically low mortgage rates. The same can be said for homeowners who decided to refinance their mortgages. Unfortunately, since mortgage rates are related to the benchmark interest rate, the era of the 3% mortgage appears to be over—at least for the foreseeable future.

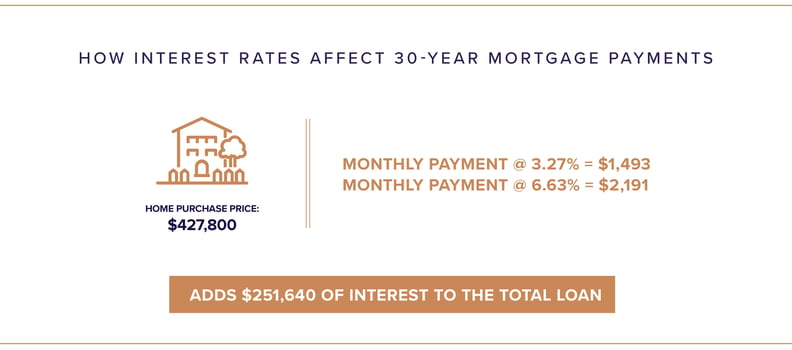

So far in 2022, we have seen the average 30-year mortgage increase from 3.27% to 6.63% as of November 30. That may be a shocking number now, but to put things into a historical perspective, mortgage rates between 5–10% were not uncommon in the 1990s and early 2000s– before 2008. Looking further back, some of our clients may remember (not so fondly) when you could expect a mortgage rate of up to 18% in the early 1980s.

So, what does this mean for today’s homebuyers in terms of dollars? Let’s consider that you’re purchasing a home for the median national average of $427,800. If we assume a 20% down payment and a mortgage on the remaining balance, the total monthly mortgage payment (principal and interest) based on today’s interest rates is $2,191. If you purchased the same home in December of last year, the payment would have been $1,493. That additional $698 per month translates to an extra $251,640 in interest over the life of the loan.

Savers.

For an investor who opted to keep their portfolio on the sidelines during this volatile year in equities and, instead, invested in money market funds, the increased interest rates have offered a bit of relief.

Between 2009 and 2021, the typical money market fund averaged an annual return of 0.40%, with most years being even less. This year, money market fund yields have increased with every interest rate adjustment, with the current yield above 3%. If rates continue to rise, these yields will rise in lockstep.

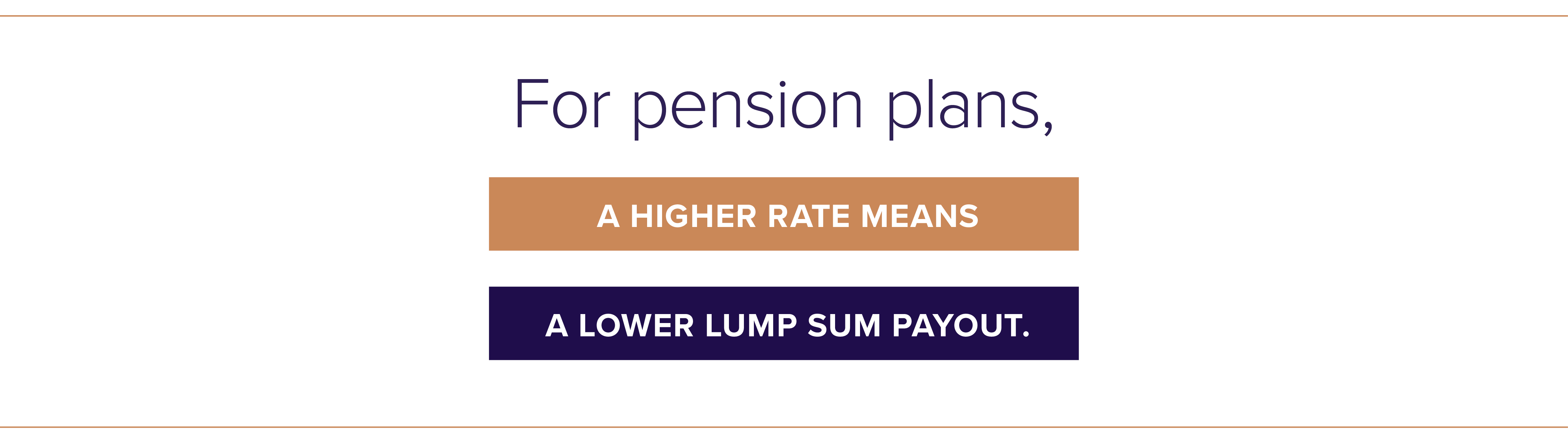

Retirees with pensions.

While investors in the accumulation phase have time for interest rates and equity values to stabilize, those approaching retirement don’t have such a luxury. Specifically, retirees with traditional pension plans– which account for roughly 15% of private-sector employees– must understand how changing interest rates affect their lump sum calculations. Since companies must use IRS-published interest rates to calculate pension lump sum, higher rates mean a lower payout.

On the other hand, pension annuities don’t fluctuate with interest rates; however, their consistent payouts are more susceptible to inflation, which is another risk we’re currently dealing with.

Investors.

Higher interest rates have been a mixed blessing for investors, especially in the bond market. The aggressive rate increases have made for larger coupon payments for newly issued bonds. Conversely, bondholders have been affected by price decreases in the bond portfolios they already own.

For investors, it has been difficult to open statements and see losses in what is typically considered the most conservative asset class, but the losses are there, and it may take a year or two for the increased interest rates to pay back the value lost in 2022. However, bond investors will benefit from higher yields in the long run.

Business owners.

Rising interest rates affect businesses in multiple ways. Most notably, high rates make it more difficult and expensive to secure loans, lines of credit, and other outside investments. This barrier to capital can stall projects and growth initiatives. Additionally, there’s the potential for lower revenue. While some industries, such as real estate and automotive, are susceptible to interest rate changes, just about every industry can feel the effects of consumers having less money at their disposal.

Where do we go from here?

It’s difficult to predict what the Fed will do next. How high will interest rates go? Could we possibly see an interest rate decrease soon? Only time will tell.

One thing we can be certain of is that interest rates are only a single factor to consider when making important financial decisions. Should you really pass on the opportunity for your dream house just because the mortgage rate is higher now than it was a year ago? Not necessarily.

As always, it’s imperative that you consider your complete financial picture rather than outweighing one aspect. If you have questions about how rising interest rates impact your financial plan, reach out to your adviser or contact Sanderson for a consultation.