On September 13, 2021, the Democratic-controlled House of Representatives’ Ways and Means Committee released their long-awaited tax legislation, the Build Back Better Act, bringing into focus the major tax changes possibly coming our way in the coming months. The proposed legislation was surprising in scope, avoiding some of the harsh provisions from Biden’s American Families Plan released earlier in the year while introducing new requirements and putting its own spin on other stipulations.

The following is a summary of the significant income tax-related proposals as they may relate to you. We will analyze the potential impact on the estate and wealth transfer landscape in a separate Insight.

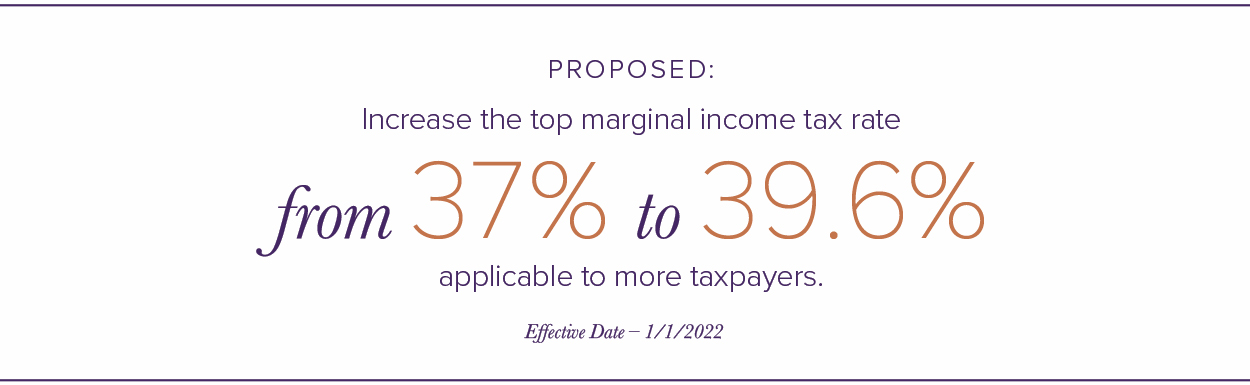

Return of the 39.6% Top Marginal Tax Rate.

The proposal increases the top marginal income tax rate from 37% to 39.6%, where it was before the Trump-era Tax Cuts and Jobs Act. More impactfully, however, the proposal would impose the new top marginal tax rate on a larger group of taxpayers. The rate would apply to ordinary income exceeding $400K for single filers and $450K for joint filers. Currently, the top tax marginal tax rate of 37% doesn’t apply until taxable income of $523,600 and $628,300, respectively, for single and joint filers. While the applicable rate and income expansion of the top marginal income tax bracket are notable, so is the compression of the gap between single and married filing joint filers. The proposal certainly exacerbates the so-called “marriage penalty” in our tax system.

3% Surtax on Modified AGI for Taxpayers.

The Act imposes a 3% surtax on income exceeding $5MM for wealthy taxpayers. Since the surtax applies to modified AGI exceeding $5MM for both single and joint filers, the tax rate on all types of income would essentially be increased for taxpayers falling within the scope of the legislation. This would push tax rates on ordinary income as high as 43.5% for earned income and 31.8% for long-term capital gains.

For trusts, the proposed legislation is even more impactful, with the 3% surtax beginning once trust income exceeds $100K. Depending on the sources of income and assets owned by the trust, the 3% surtax could represent a significant increase in tax liability, particularly for those owning business interests or accumulating retirement benefits. Tax-efficient beneficiary distribution planning will become even more important and complicated for trustees as a result.

Immediate 2020 Tax Rate Increase on Long-Term Capital Gains.

The Act imposes a 25% tax rate on long-term capital gains for taxpayers in the new top tax bracket ($400K for single, $450K joint filers). Currently, the top tax rate is 20% for these filers and begins at slightly higher thresholds of $445,850 (single) and $501,600 (joint). With the exception of gains from certain binding contracts previously entered into, the new rate would apply to all realized long-term capital gains occurring after 9/13/2021. This would essentially eliminate any year-end gain recognition planning for taxpayers in response to the law changes.

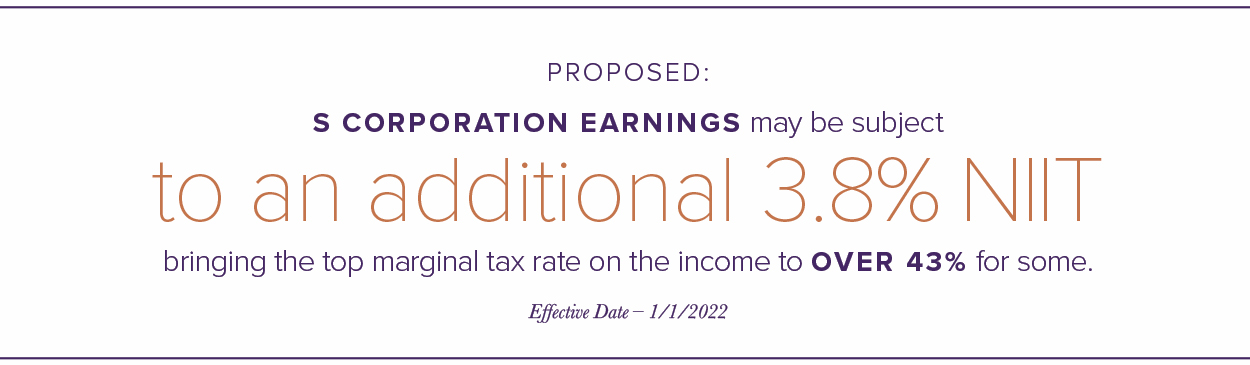

3.8% Net Investment Income Tax Application to S Corporation Owners.

S corporation owners can currently shield pass-through income from the S corporation from both self-employment taxes and the 3.8% Net Investment Income Tax. However, the Build Back Better Act proposal significantly changes this for some owners with “Specified Net Income” from their S corporation and regular investments. For taxpayers with modified AGI over $400K (single) or $450K (joint), S corporation earnings may be subject to the additional 3.8% NIIT, bringing the top marginal tax rate on the income to over 43% for some. There is a $100K phase-in range for taxpayers slightly over the thresholds noted above, but generally, the proposed legislation represents a major tax increase for successful S corporation owners when coupled with the rate changes noted previously.

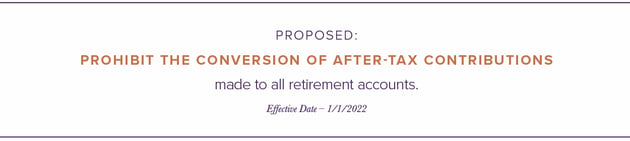

Elimination of Backdoor Roth IRAs.

The proposed legislation would prohibit the conversion of after-tax contributions made to all retirement accounts, including employer-sponsored plans like 401(k)s. Currently, taxpayers over the income threshold for making direct contributions to Roth IRAs can make nondeductible contributions to regular IRAs and immediately convert them to Roth IRAs without causing any increase in their income tax liability (assuming they have no other pre-tax retirement assets that would cause pro-rata inclusion in tax income on the conversion). As a result of this legislation, taxpayers phased out of making Roth IRA contributions would no longer have the backdoor contribution work around, leaving their only option to build a Roth IRA as the taxable conversion of pre-tax assets…for now.

Roth Conversion Prohibition.

For taxpayers with taxable income in excess of $400K (single) and $450K (joint), the ability to do a Roth conversion at all is prohibited under the legislation. However, the provision would not apply until 2032, giving impacted taxpayers plenty of time to convert their IRA assets to Roth IRAs should they want to voluntarily pay the income taxes early in this Biden-era period of high taxation.

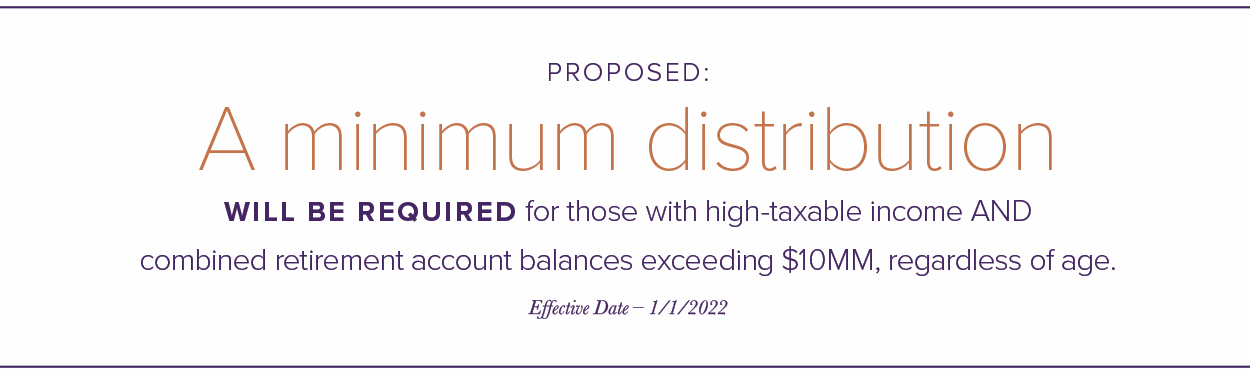

Super-charged RMDs for High-Income Taxpayers.

For individuals with high-taxable income ($400K single and $450K joint) AND combined retirement account balances exceeding $10MM, a required minimum distribution will be necessary for the year, regardless of the taxpayer’s age. The RMD will equal 50% of the combined account value over $10MM and 100% of the value over $20MM. These same taxpayers would be prohibited from making any additional IRA contributions for the year as well.

Our observations.

The income tax proposals included in the Build Back Better Act represent a dramatic tax increase for high-income taxpayers. While ultra-wealthy taxpayers certainly bear a heavy burden under the proposal (i.e., the 3% surtax on MAGI and retirement account RMDs), “mere mortal” taxpayers earning $400K/$450K are squarely in the crosshairs of the tax legislation, and if imposed, will be the ones to feel the impact of the proposed legislation the hardest in their wallets. The compressed marriage penalty disparity between single and joint filers, along with the new top marginal tax rates on ordinary income and long-term capital gains, will undoubtedly be felt by taxpayers caught in the biggest gap between the current tax landscape and the proposed new laws.

While the legislation still has many obstacles to overcome before it becomes law, and changes to some of the provisions are inevitable, one thing seems certain. A majority of our clients should be prepared for a substantial increase in their tax burden and be prepared, to the extent possible, to accelerate planning opportunities before the end of the year once final legislation starts to take shape. If the proposed Build Back Better Act is any indication, the window to do so will likely be brief.