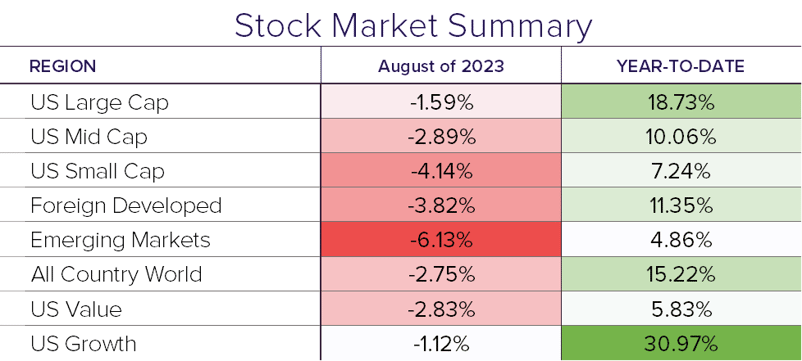

A tepid August broke a five-month streak of gains for the S&P 500 as it finished negative 1.59%. The sell-off extended across the globe as foreign developed stocks and emerging market stocks both finished lower as well. The bond market was also affected as it finished down 0.6%. Conflicting economic data, a U.S. credit rating downgrade, rising rates, and China growth concerns all contributed to a volatile August.

Economic News

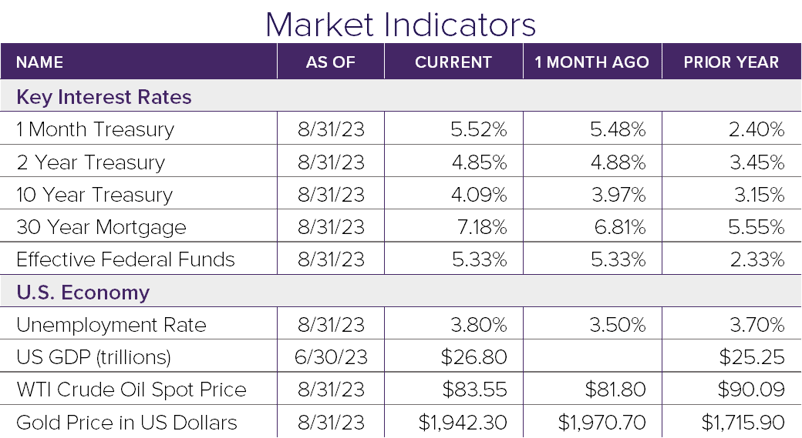

At the start of August, the U.S. government credit rating was downgraded by rating agency, Fitch Ratings, from the AAA to AA+. Fitch cited rising debt and a “steady deterioration in standards of governance over the past 20 years.” This downgrade initially had little effect on interest rates and markets; however, interest rates began to climb on mixed economic data.

U.S. Inflation inched higher while core inflation (less food and energy) fell slightly. The U.S. PMI, a key manufacturing index, rose slightly to 47.6 but remains under the key 50 level. A reading of less than 50 indicates the index is in a state of contraction. On the housing front, existing homes sales dropped for the 16th month out of the last 18, while new homes sales increased 4.4%. The average 30-year mortgage rate reached 7.23% in August, the highest level in over 20 years.

Markets and Rates

In addition to this mixed data, there are indications from the Federal Reserve that a higher-for-longer interest rate scenario may be warranted. The 10-year treasury spiked to 4.35% after starting the month under 4%. The rising bond yields ultimately put pressure on stocks.

Fast growing technology and growth stocks are very sensitive to higher interest rates. With much of this year’s gains being attributed to the Magnificent Seven (Microsoft, Telsa, Nvidia, Apple, Google, Facebook, and Amazon) it’s no surprise that we saw the S&P give up 1.59%. Small and mid-cap stocks also contracted 4.1% and 2.9%, respectively. Emerging Markets were worse off for the month thanks to some major concerns out of China. The China-heavy index dropped 6.1% in August.

Looking Ahead

Seasonally, September is not a great month for the markets. It will be important to keep an eye on the economic data stream and additional comments from the Fed for any clarity around interest rates. In the meantime, enjoy the start of fall.